Note: This guide may be amended based on the Pension Protection Act.

Please visit the Glossary of Pension Terms for definitions of the terms used in this Guide. Also, a Guide to Understanding Your Pension Plan includes helpful links to:

- How FSRA regulates pension plans

- An overview of the retirement income system

- How registered pension plans work

- How life events can impact your pension benefits

Perhaps you’ve heard the company that funds your workplace pension is in financial trouble or is bankrupt or insolvent. Your pension plan could be underfunded because your employer is not able to make payments to your pension plan. This could mean there’s not enough money in the pension fund to pay all the pension benefits you are owed.

If your employer is insolvent, they may restructure under the Companies’ Creditor Arrangement Act (CCAA). If your employer stops operating during the CCAA process, or declares bankruptcy under the Bankruptcy and Insolvency Act, FSRA will appoint an Administrator to mange the plan and order the wind up of the plan. The appointed Administrator can also advance claims on behalf of the plan members.

There are also times where members, or member groups, obtain their own legal representation where the plan is underfunded. Legal representation could also be obtained to advance other claims in the bankruptcy process.

This guide is about what happens to your pension plan if your employer is bankrupt or stops operating, and your pension plan is wound up. This guide does not address restructuring.

It can take several months or years to wind up a pension plan, based on the plan’s size and complexity. This can be a very challenging and uncertain time for you until the plan is fully wound up. Depending on the type of pension plan you have, the process and protection may be different.

Top tips to stay engaged with your pension plan if your employer is insolvent:

Tip 1: If you have moved recently, provide the appointed pension plan Administrator with your contact information and current address.

Tip 2: Review and respond to all communications sent to you by the pension plan Administrator within the set timelines.

Tip 3: If you have not received communication from the pension plan Administrator, contact them and confirm they have your current address and contact information. Before a plan sponsor is bankrupt, the Administrator is required to provide:

- annual pension statements to plan members

- statements to former or retired members every two years

- termination statements to former members with deferred pensions

After bankruptcy, the Administrator will provide you with correspondence about the wind up process and a personalized option form.

Tip 4: If you do not know who your pension plan administrator is or how to contact them, FSRA can provide you with this information: Contact FSRA.

Insolvency occurs when your employer cannot meet their debt payments on time.

Bankruptcy is a legal process that happens when your employer declares they can no longer pay back their creditors.

Restructuring, under the Companies’ Creditors Arrangement Act (CCAA), is short-term protection from creditors given to companies so they can reorganize their business and financial affairs, typically while under financial hardship.

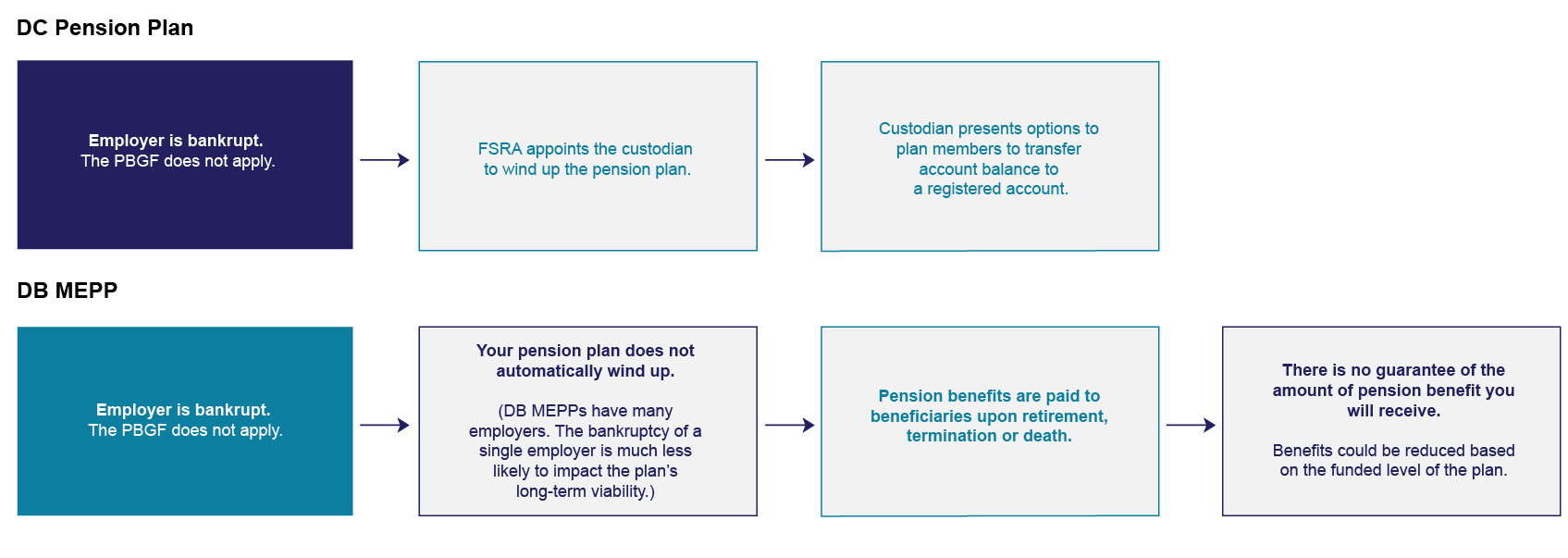

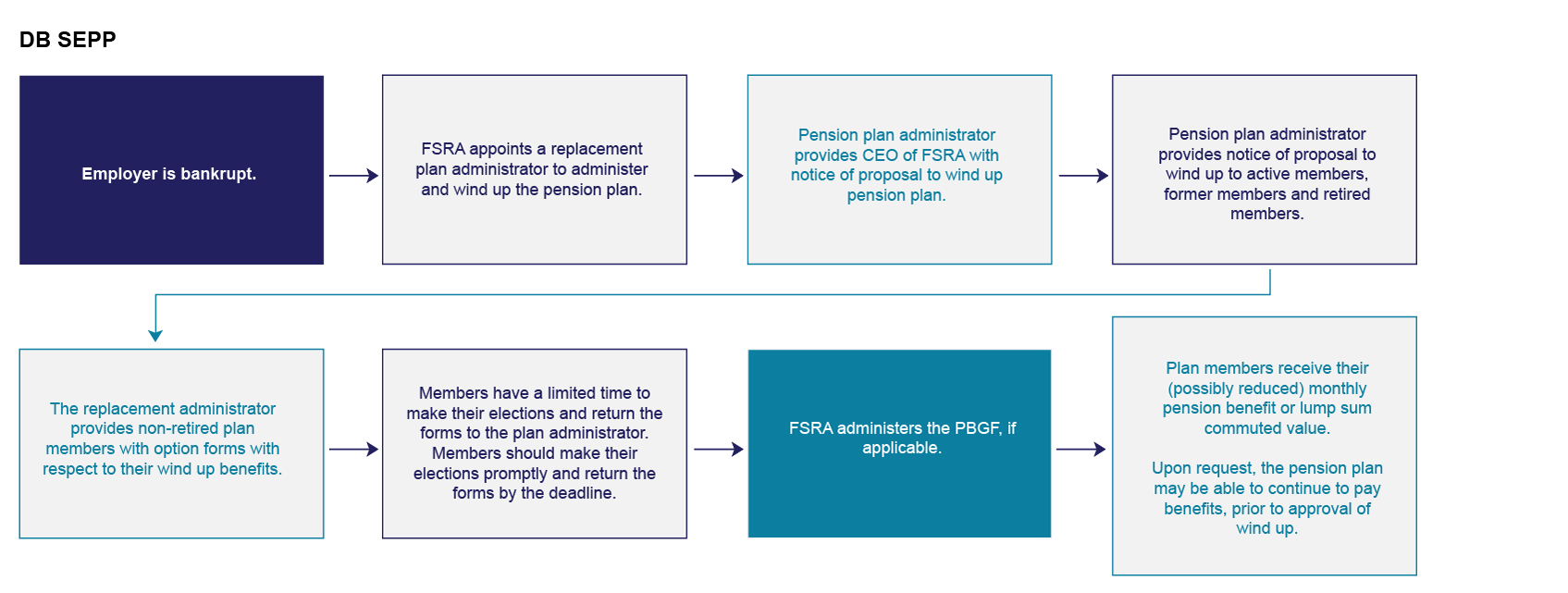

Bankruptcy journey by Pension plan type

What is the difference between “solvency” and “going concern”?

Solvency refers to the funding a pension plan needs to pay all benefits owed to its members assuming it is wound up today. Going concern assumes the pension plan will continue indefinitely.

Depending on the type of pension plan you have, the process and protection may be different if your employer is bankrupt. You can find out what type of pension plan you have by looking-up your pension plan and check your benefit type online.

With Defined Contribution (DC) Pension Plan or Defined Benefit Multi-Employer Pension Plan (DB MEPP), there is no guarantee of the amount of pension benefit you will receive. For DC pension plans, if your employer is bankrupt, your pension benefit will generally be paid at the balance in your account. For multi-employer pension plans, the plan may continue, if there are other participating employers not bankrupt.

Image

If you have a Defined Benefit (DB) Single Employer Pension Plan (SEPP), the funded level (i.e., solvency) of your pension plan may impact your pension benefit. If your pension plan is not fully funded (i.e., is less than 100% funded on a solvency basis) when it is wound up, your pension benefits may be at least partially protected by the Pension Benefit Guarantee Fund (PBGF). To learn more about the PBGF, please refer to the Appendix.

Under Ontario’s pension standards legislation, the Pension Benefits Act, most DB SEPPs are required to fund their plan to 85% on a solvency basis and 100% on a going concern basis. If they fall below that, your employer may have to make special payments. These special payments are made over an amortization period of a number of years. The shortfall is not immediately eliminated.

Image

Stay informed about your pension plan

- Ask questions. For most questions about your pension plan, your first point of contact is the pension plan administrator. This does not change whether you have left your employer or are retired.

- Find out what type of pension plan you have and check your benefit type online.

- If you are a DB plan member, review your annual pension plan statement. It will show you information about your pension benefit as of the statement date. Keep in mind that this information may change at the time the pension plan is being wound up:

- The funded status of your pension plan. Keep in mind the funded status may have changed since the annual statement was issued.

- Whether your plan sponsor was making special payments to pay off a deficit in the pension plan.

- The Transfer Ratio, which indicates the degree to which a pension plan has sufficient funds to provide pension benefits.

- A ratio of less than 1.0 means that your pension plan does not have enough funds to pay its pension benefits. This could mean a reduced pension if the plan is wound up (i.e., not while a going concern).

- You can ask your plan administrator what steps they’re taking to ensure the transfer ratio gets closer to 1.0.

- As a plan member, you are entitled to certain information about your pension plan and can view plan documents. To review any plan documents or ask about the funded status of your DB pension plan, contact your plan administrator.

- Review the FSRA website. It contains useful resources for pension plan members, including questions and answers related to pension benefits in Ontario.

Appendix

What is the Pension Benefit Guarantee Fund (PBGF)?[1] The PBGF is a fund administered by FSRA to cover pension benefits for certain defined benefit pension plans if they are wound up due to employer bankruptcy and there is a funding shortage.

The plan wind up and PBGF processes are overseen and approved by FSRA. The PBGF pays into the pension plan during the wind up process before member benefits are paid. It does not pay plan beneficiaries directly.

Ontario is the only jurisdiction in Canada with such a fund. The PBGF was established in 1980. Since inception, it has paid $1.7 billion in claims, providing a safety net to many plan beneficiaries. The PBGF is funded by assessments paid by pension plan sponsors. However, in the past, when the PBGF has not had enough funds to pay claims, the government has granted and loaned money to the PBGF. In 2009, the PBA was amended to clarify that the government is not obligated to make a loan or grant to the PBGF.

Key elements of the PBGF

- The PBGF is funded by assessments paid by employers.

- The assessment level and benefit amount are prescribed under the Pension Benefits Act (PBA).

- The PBGF may apply where an employer becomes bankrupt, and there is a funding shortfall in the pension plan.

- The PBA limits how much the PBGF can pay out based on the funds it holds at a given time.

- The Ontario Government is not obligated to make a loan or grant to the PBGF.

- The CEO of FSRA is the administrator of the PBGF and administers and invests the fund.

Who is covered by the PBGF? With some exceptions, if you belong to a defined benefit pension plan sponsored by a single employer and earned benefits while working in Ontario, your pension benefits may be covered by the PBGF. Your benefits may be covered even if the pension plan is registered in a different province, provided you were employed in Ontario.

Even with PBGF protection, pension promises may not be fully honoured if your employer becomes bankrupt.

Not all pension plan types are covered by the PBGF. The PBGF does not cover:

- Multi-employer pension plans

- Jointly sponsored pension plans

- Individual pension plans

- Defined contribution pension plans

- Pension plans that have existed for less than five years

Benefit improvements to PBGF-eligible pension plans made less than five years before the plan winds up are not covered by the PBGF.

How much of my pension benefit is covered by the PBGF if my employer is bankrupt? Regulations set out the amount of benefits payable by the PBGF. The maximum benefit amount that is made whole with PBGF funds is currently set at $1,500 per month. The pension amount above $1,500 per month is reduced by the Transfer Ratio in the wind up valuation.

Sample calculations of the amount of benefit paid by the PBGF are shown in three examples below, for demonstration purposes only:

- In all cases, the pension plan is assumed to be 80% funded on a solvency basis (i.e., Transfer Ratio = 0.80) and the PBGF is fully funded.

- In Example 1, the member’s monthly pension benefit is $1,100.

- In Example 2, the member monthly pension benefit of $1,500.

- In Example 3, the member’s monthly pension benefit is $2,500.

Example 1

- CEO of FSRA declares the PBGF applies to the pension plan.

- The pension plan is 80% funded on a solvency basis.

- The member has a total pension of $1,100 per month.

- The pension plan pays the pension based on its funded ratio (80% of $1,100, or $880).

- The PBGF allocates funds to the pension plan. The pension plan pays up to the maximum benefit ($1,500) not covered by the pension plan (20% of $1,100, or $220).

- The entire pension benefit of $1,100 per month is payable after wind up.

| Example 1 – Calculation | |||

|---|---|---|---|

| Benefit payable | Payable by plan at funded ratio of 80% | Payable from the PBGF at 20% | Total payable |

| On 1st $1,500 of monthly pension | $880 (80% x 1,100) | $220 (20% x 1,100) | $1,100 |

| On excess over $1,500 ($0) | Nil | Nil | Nil |

| In total | $880 | $220 | $1,100 |

Example 2

- CEO of FSRA declares the PBGF applies to the pension plan.

- The pension plan is 80% funded on a solvency basis.

- The member has a total pension of $1,500 per month.

- The pension plan pays the pension based on its funded ratio (80% of $1,500, or $1,200).

- The PBGF allocates funds to the pension plan. The pension plan pays the maximum benefit ($1,500) not covered by the pension plan (20% of $1,500, or $300).

- The entire pension benefit of $1,500 per month is payable after wind up.

| Example 2 – Calculation | |||

|---|---|---|---|

| Benefit payable | Payable by plan at funded ratio of 80% | Payable from the PBGF at 20% | Total payable |

| On 1st $1,500 of monthly pension | $1,200 (80% x 1,500) | $300 (20% x 1,500) | $1,500 |

| On excess over $1,500 ($0) | Nil | Nil | Nil |

| In total | $1,200 | $300 | $1,500 |

Example 3

- CEO of FSRA declares the PBGF applies to the pension plan.

- The pension plan is 80% funded on a solvency basis.

- The member has a total pension of $2,500 per month.

- The maximum benefit of $1,500 from the PBGF is payable at 80% by the pension plan and 20% by the PBGF.

- In addition, the pension plan pays for the excess of the member’s total pension over $1,500 at its funded ratio (80% of $1,000, or $800).

- In total, the pension plan pays $2,000 (80% of $2,500). The PBGF allocates funds to the pension plan and the pension plan pays $300 (20% of $1,500).

- A pension benefit of $2,300 per month is payable after wind up.

| Example 3 – Calculation | |||

|---|---|---|---|

| Benefit payable | Payable by plan at funded ratio of 80% | Payable from the PBGF at 20% | Total payable |

| On 1st $1,500 of monthly pension | $1,200 (80% x 1,500) | $300 (20% x 1,500) | $1,500 |

| On excess over $1,500 ($1,000) | $800 (80% x 1,000) | Nil | $800 |

| In total | $2,000 | $300 | $2,300 |

How is the PBGF funded? The PBGF is funded by all employers who sponsor defined benefit pension plans and who qualify for this coverage. They are responsible for making yearly payments into the PBGF, based on the pension plan’s financial status and the number of Ontario plan beneficiaries who are part of the pension plan.

How are payments to the PBGF made? Plan administrators complete an annual PBGF Assessment Certificate as prescribed under the regulation of the PBA. It sets out the calculation of the PBGF assessment[2] on the funded level (i.e., solvency) of the pension plan and the number of Ontario members covered under the plan. The larger the plan’s solvency shortfall, the larger its PBGF assessment.

How many claims are made to the PBGF each year? For how much? On average, five claims are made per year. The claims are generally small. The total amount paid out of the PBGF is about $31 million per year. Larger claims occur less frequently.

How is the PBGF invested? The PBGF is invested prudently and to ensure it can pay out potential claims and cover expenses incurred as part of its administration. Currently the assets are invested 56% in a money market fund and 44% in short-term, high-quality government bonds.

What happens if there are no funds left in the PBGF when my employer goes bankrupt? The PBGF's ability to pay benefits is limited to available funding. The PBGF does not have an ability to seek loans. In the past, in large bankruptcies, the government has provided loans and grants to the PBGF, but there is no obligation for it to do so.