Market conditions

Market conditions are factors that continually change and influence the cost of auto insurance and the price you pay. Several factors are driving up costs such as inflation and the impact it is having on items like auto parts and the cost of labour. Another factor is that people are driving more and there are more cars on the road increasing the risk of an accident. Increasing rates of auto theft can also impact your premium. FSRA will continue to actively monitor these conditions and the potential impacts they will have on auto insurance rates.

The impact of these factors may be widespread or specific to your local area. Examples of current market conditions affecting auto insurance premiums in Ontario include:

Image

Auto theft

Increasing rates of auto theft in Ontario can impact your auto insurance premium.

According to our expert benchmark report, there was a 65% increase in theft claim costs in 2021. We expect theft claims costs to continue to increase.

Insurance companies consider the risk of theft when determining insurance rates. It’s important to stay informed, shop around, and talk to your insurance company about incentives, rebates or discount programs for installing anti-theft devices or other risk control measures.

Image

Inflation

Your premium is affected by the increase in the price of goods, services and labour over time. Insurers adjust premiums based on the expected cost of covering future auto insurance claims.

Based on Statistics Canada data, consumer prices increased by 3.3% year-over-year in July 2023. Despite a decline in general inflation, there is a noticeable and significant upward trend in inflation related to auto insurance physical damage. Ontario has seen an 8.1% increase in the cost of vehicle parts, maintenance and repairs. This sharp increase impacts the costs of auto physical damage claims.

Image

Physical damage costs

New technology has increased the cost of fixing vehicles. For example, most cars now have rear view cameras and sensors in their back bumper. This means the repair includes not just the bumper, but the technology in the bumper as well.

In the past 5 years, physical damage costs per claim increased by 22.5% and continues to increase at a rate of 7.4% per year. These increases can be explained by the rising price of automobile parts and escalating labour cost.

Image

Drivers on the road

A change in how much we drive also has an impact on premiums. For example, more cars on the road results in more collisions and higher claims costs.

There is a growing cost pressure in the auto insurance market as more vehicles are on the roads.

Data from our expert benchmark report shows that Ontarians’ driving behaviour is now gradually returning to pre-pandemic levels, meaning more drivers are on the road.

COVID

During the COVID pandemic, there were unprecedented changes in market conditions. There was a significant drop in the number of collisions and claims because people were staying home and driving less. To address this, FSRA created pathways to enable insurers to quickly adjust their rates.

Through these pathways, auto insurance rates were reduced for many drivers in the province as insurers voluntarily gave back over $1.8B to policyholders. FSRA approved 108 emergency rate reductions and 45 emergency premium rebates as of April 2022. View private passenger automobile emergency relief for a list of all emergency rate reductions and rebates during the pandemic.

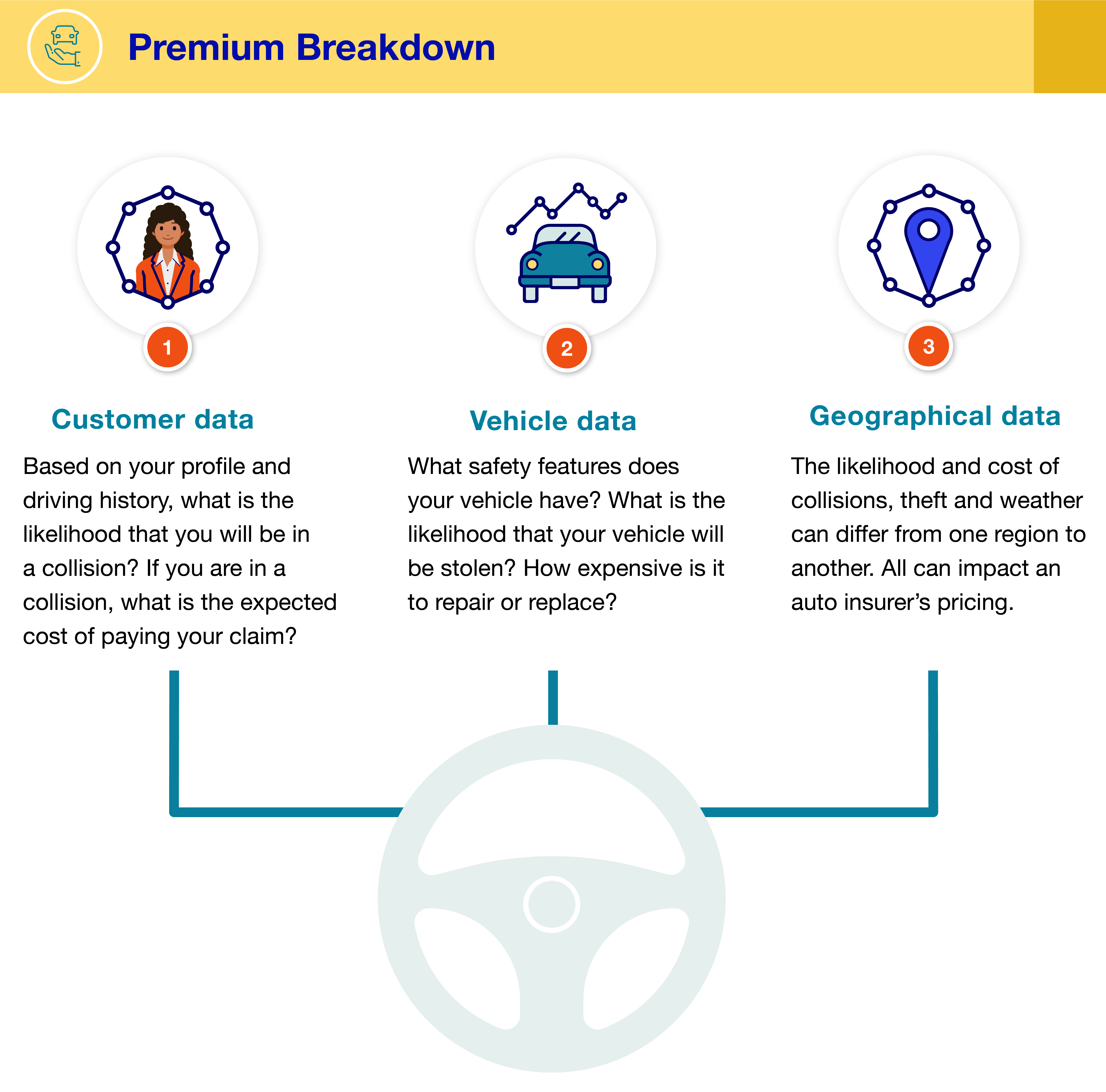

Other factors that impact your auto insurance premiums

By far, the largest percentage of auto insurance costs relate to the likelihood of being in a collision and paying out claims. Drivers with recent driving convictions, a history of at-fault claims or limited experience generally represent a higher risk than drivers with “clean” driving records and many years of driving experience. As a result, those drivers deemed to be a higher risk typically pay more.

To get the best price for your auto insurance FSRA encourages consumers to shop around. And, if you have good driving habits, usage-based insurance can possibly save you more.

Learn more about how to save on auto insurance.