Table of contents

Executive summary

About us

Sectors we regulate

FSRA's complaints process

What happens to more serious cases?

What complaints we do not handle

Fiscal year 2021/22 in review

Mortgage brokering

Auto insurance

Property and casualty insurance

Life and health insurance

Credit unions and caisses populaires

Health service providers

Loan and trust companies

Appendix: FSRA service standards - complaints

Executive summary

The Financial Services Regulatory Authority of Ontario (FSRA) is an independent regulatory agency created to improve consumer and pension plan beneficiary protections in Ontario. FSRA's mission is to provide public service through dynamic, principles-based and outcomes-focused regulation. The organization's vision is to promote financial safety, fairness, and choice for Ontarians and for them to have their complaints resolved in an accessible, fair, timely, transparent, and effective manner.

By receiving complaints from members of the public, FSRA is assisted by consumers to maintain high standards of conduct in the regulated sectors and better protecting consumers from harm. When a consumer shares their experience through complaints, it enables FSRA to identify trends and share them with other departments within the organization. Complaint trends inform FSRA’s business planning and priorities. They may also trigger regulatory activity, including disciplinary action or proactive reviews of licensees, legislative changes, and public awareness and educational campaigns.

How FSRA protects consumers through complaint handling

FSRA’s Complaints and Risk Assessment Unit (CRAU) handles complaints against individuals and entities that are licensed or should be licensed by FSRA in the following regulated sectors:

- auto insurance

- credit unions and caisses populaires

- financial planners and financial advisors

- health services providers (related to auto insurance)

- life and health insurance

- loan and trust companies

- property and casualty insurance

- mortgage brokering

*The Pensions Department handles Pension Plan complaints.

The CRAU performs an essential role in assisting the agency in understanding how our regulated sectors are performing and whether those individuals and entities are conducting themselves in a fair and compliant manner. The CRAU also provides the public with an open and responsive avenue for complaint handling.

The CRAU reviews complaints ranging from simple matters, such as something that can be resolved by the licensee and consumer to complex ones requiring us to examine numerous documents and corroborate the evidence between the complainant and the licensee. All complaints are reviewed with the same level of due diligence, regardless of their complexity.

Top complaint themes in 2021-2022

Image

Our office closed 857 complaints during fiscal year 2021/22 (April 1, 2021 to March 31, 2022). A key performance indicator is to manage caseloads by balancing the number of complaints closed versus new complaints received during the reporting period. Due to the timing of complaints received and the level of complexity involved in some cases, files closed in the reporting period may have been carried over from a prior year. For this fiscal year, the team closed 13 more complaints than received. That’s a closing rate of 102% of complaints received. Similarly, in the last three fiscal years, FSRA received an average of 992 complaints and closed 1,016 complaints.

We categorize complaints by themes to help us monitor market behaviour by reviewing patterns of systemic issues, sector-specific risks, and overall industry compliance. Here are the top complaint themes for complaints FSRA closed during fiscal year 2021/22 in each sector.:

| Sector | Top complaint theme |

|---|---|

| Mortgage Brokering | Contractual matter |

| Auto Insurance | Claims and Settlement |

| Property and Casualty Insurance | Claims and Settlement |

| Life and Health Insurance | Regulatory Action in Other Jurisdictions |

| Credit Unions and Caisse Populaires | Customer Service |

| Health Service Providers | Administration |

| Loan and Trust Companies | Contractual matter |

About us

FSRA is an independent regulatory agency created to improve consumer and pension plan beneficiary protections in Ontario. The authority was launched in June 2019 to replace the Financial Services Commission of Ontario (FSCO) and the Deposit Insurance Corporation of Ontario (DICO). The agency is flexible, self-funded, and designed to respond rapidly to an evolving commercial and consumer environment.

In this capacity, FSRA:

- promotes high standards of business conduct

- fosters a sustainable, competitive financial services sector

- responds to market changes quickly

- promotes good administration of insurance and pension plans

- encourages innovation

Image

Sectors we regulate

FSRA protects Ontarians by regulating the following sectors:

- auto insurance

- credit unions and caisses populaires

- financial planners and financial advisors

- health services providers (related to auto insurance)

- life and health insurance

- loan and trust companies

- pension plan administrators[1]

- property and casualty insurance

- mortgage brokering

FSRA's complaints process

FSRA's Complaints and Risk Assessment Unit (CRAU) is the single point of contact for complaints regarding FSRA's regulated sectors, except pension plans. Consumer complaints provide a snapshot of how actual market outcomes are experienced by consumers when they use the services and products of our regulated sectors. By analyzing information provided by consumers and industry about the financial services marketplace, FSRA can assess whether the regulatory expectations contained in legislation regarding consumers have been met.

FSRA's regulated entities are required to have effective and transparent protocols to resolve complaints that are submitted directly to them. Where complaints cannot be resolved, a consumer after considering other avenues such as a third-party dispute resolution body,[2] may elect to come to FSRA.

Image

When a complaint is submitted to FSRA, in most cases it is expected that a consumer would have received a final decision in writing from the person or entity with which they have a concern. That final decision should be part of the material included with the complaint submitted to FSRA. This allows FSRA to review a complaint quickly with an understanding of the position and available documents of both parties. It also ensures that our licensees are documenting complaints and making real attempts to evaluate and resolve complaints against them.

Image

For all complaints, FSRA sends an acknowledgement of receipt letter to the complainant, and a Compliance Officer in the CRAU is assigned to the complaint. The Compliance Officer assigned to the case reviews the allegations in the complaint and makes initial contact with the complainant to ensure a clear understanding of the allegations.

Image

During the review, the Compliance Officer will collect evidence from the complainant, licensee and if appropriate, other parties involved, to determine if the allegations in the complaint support a breach under the legislation, regulation and/or relevant codes of conduct.

Based on the allegations and evidence collected during the review, we will let the complainant know of the determination through a closing letter. Outcomes may include:

- a case was closed because the information provided was insufficient to render a decision

- A determination that FSRA is not the regulatory body with authority over the issue presented or the licensee who is the subject of the complaint. Staff will provide the complainant with appropriate options for alternative resolutions, if they wish to pursue their complaint.

- a decision that confirms that the information provided indicates the licensee was compliant

- In the case of non-compliance, the consumer is informed that the review is complete. Appropriate action will be taken with the subject of the complaint, such as issuing a warning letter.

- where more serious outcomes are suspected, complaints may be escalated to other areas of FSRA for consideration of other regulatory outcomes within Market Conduct or to FSRA's Legal and Enforcement (L&E) Department

- Contractual matters are reviewed to ensure that the licensee has carried out the terms of the contract in the stated and agreed upon way. Disagreements regarding contractual outcomes where adherence is not an issue, such as the amount of a total loss, or bodily injury settlement would not be within FSRA’s jurisdiction. However, in these cases we may provide alternatives to a consumer where such disputes may be continued.

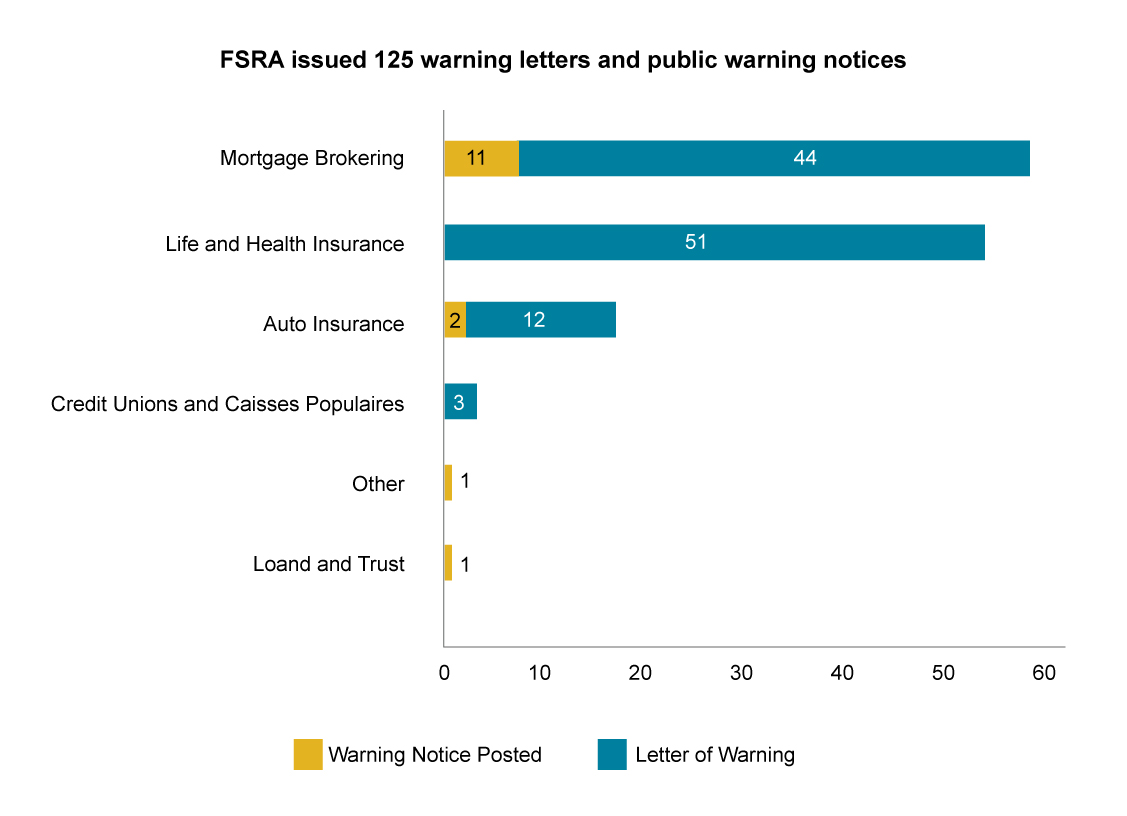

During this fiscal year, the CRAU issued 110 Warning Letters to individuals or entities found in contravention of the legislation and the Acts we supervise to address this misconduct. Our office also published 15 public notices warning consumers about unlicensed activity and the risk of engaging in business with unlicensed individuals and entities.

Image

In cases where the outcome of our review includes an assessment that the licensee is compliant, but the practice or activity of the licensee has the potential for consumer harm, the CRAU educates the licensee and makes recommendations regarding improved consumer outcomes and compliance culture.

The CRAU reviews all complaints with the same level of due diligence regardless of the outcome. In addition to complaints made to FSRA by consumers, the CRAU also initiates reviews from information obtained from other sources, such as sanctions imposed by other regulators, government, media reports, and industry reports.

What happens to more serious cases?

Image

In cases of multiple or severe compliance infractions, the CRAU escalates the matter to our L&E Department for consideration of regulatory sanctions, such as non-renewal, cancellation, conditions on a license, suspension, revocation, or administrative monetary penalties. Personnel within Market Conduct may also receive escalations from CRAU for cases requiring license conditions or other penalties related to administrative contraventions.

Image

For referrals to L&E, FSRA has a governance structure that ensures consistent risk criteria are applied to the escalation of the most serious files. Risk criteria include breaches of legislation causing consumer harm, repeated non-compliance or disregard for operating within the regulatory regime, or misconduct that FSRA has stated will be targeted for review as part of its business priorities. Sometimes complainants are asked to participate in the enforcement process by providing witness testimony; otherwise, FSRA does not communicate with complainants once the file is escalated for further investigation until such matter becomes public. For more information on FSRA's Enforcement Actions and when matters become public, please see our Transparent Communication of FSRA Enforcement Action Guidance.

FSRA's L&E Department issues Notices of Proposals (NOP) that contain allegations of serious conduct and a recommended outcome. Outcomes can include license refusals, suspensions, revocations, conditions, and recommended administrative monetary penalties. Licensees, or in some cases, applicants to become licensees, have 15 days to decide to have their matter heard before the Financial Services Tribunal (FST). FST is an independent, adjudicative body with exclusive jurisdiction to determine all questions of fact or law that arise in any proceeding before it. For those who do not proceed to a hearing, FSRA issues an Order to impose the terms outlined in the NOP.

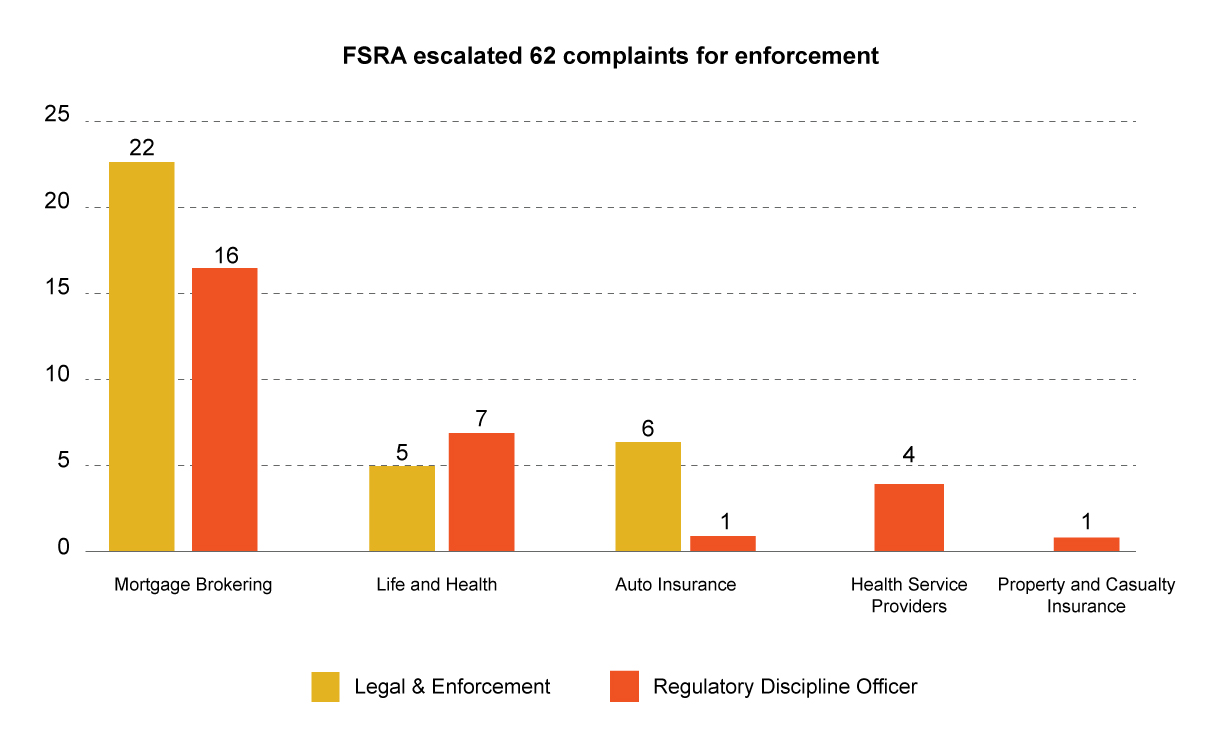

The following complaints were escalated within Market Conduct to Regulatory Discipline Officers (RDOs) and to the L&E Department in Fiscal Year 2021/22:

Image

To learn more about complaints submitted against life agents, please see the 2020/21 Life Agent Reporting Form (LARF) Summary Report.

In summary, the complaints process facilitates the maintenance of high standards of conduct in the regulated sectors and protects individuals from consumer harm. When evidence shows that a licensee has not been compliant with the relevant legislation or regulations, appropriate enforcement action is taken based on specific case facts and circumstances of the conduct and may result in any of the following outcomes:

- best practice letter to educate

- warning letter

- administrative monetary penalty and/or fine

- compliance order

- posting of a public warning notice

- conditions attached to license such as enhanced supervision, limit on activities, etc

- suspension or revocation of a license that bans, permanently or for a specified period, from conducting business in the regulated sector

- other remedies or penalty deemed appropriate

The CRAU tracks these outcomes to understand whether or not licensees are meeting consumers' expectations. Where we find emerging risks, FSRA considers the impact and how it may influence future work planning. The information provided in the complaints enables the CRAU to identify trends and share information with other departments within the organization. Complaint trends impact proactive supervisory initiatives, inform rulemaking, and are considered when making legislative changes and releasing public awareness bulletins.

What complaints we do not handle

Image

FSRA's complaint handling does not include intervening in claims settlement amounts or assisting with recovering money lost through services offered by licensees. In the Insurance sector, consumers can have certain decisions regarding claims settlements reviewed by third-party dispute resolution bodies[1] that Insurance companies must be members of. Otherwise, a civil court of law can decide on cases of negligence and/or contractual disputes and award judgments that make complainants whole. However, every complaint is reviewed to get to the point of understanding the appropriate outcome and communicating it to the consumer. Regardless of the outcome, complaint resolution assists us with monitoring conduct in our regulated sectors and understanding if further rules or guidance should be considered to keep pace with industry trends and continue to carry out FSRA's vision of financial safety, fairness, and choice for all Ontarians.

Fiscal year 2021/22 in review

Here is a sectoral breakdown of complaints that FSRA received and closed for fiscal year 2021/22:

| Sector | Complaints received | Complaints closed |

|---|---|---|

| Mortgage Brokering | 279 | 273 |

| Auto Insurance | 230 | 239 |

| Life and Health Insurance | 177 | 181 |

| Property and Casualty Insurance | 83 | 84 |

| Credit Unions and Caisse Populaires | 39 | 40 |

| Other | 15 | 15 |

| Health Service Providers | 10 | 15 |

| Loan and Trust Companies | 11 | 10 |

| Total | 844 | 857 |

The average time to complete a review of a complaint was 47 days, where 92% of our cases were closed within 120 days, and 98% were closed within 270 days.

Mortgage brokering

FSRA licenses all mortgage brokers, agents, brokerages, and administrators, a mandatory requirement for dealing and trading in mortgages within Ontario. The regulatory regime helps build a solid foundation for homeowners, investors, and mortgage providers. As part of the regulatory regime, all FSRA-licensed mortgage professionals are also held accountable to Industry Codes of Conduct and FSRA Guidance. Examples include:

- MBRCC's Code of Conduct for the Mortgage Brokering Sector

- new mortgage agent and broker licensing requirements

- licensing exemption for permitted clients that are not Individuals

- MBRCC Cybersecurity Guidance

Image

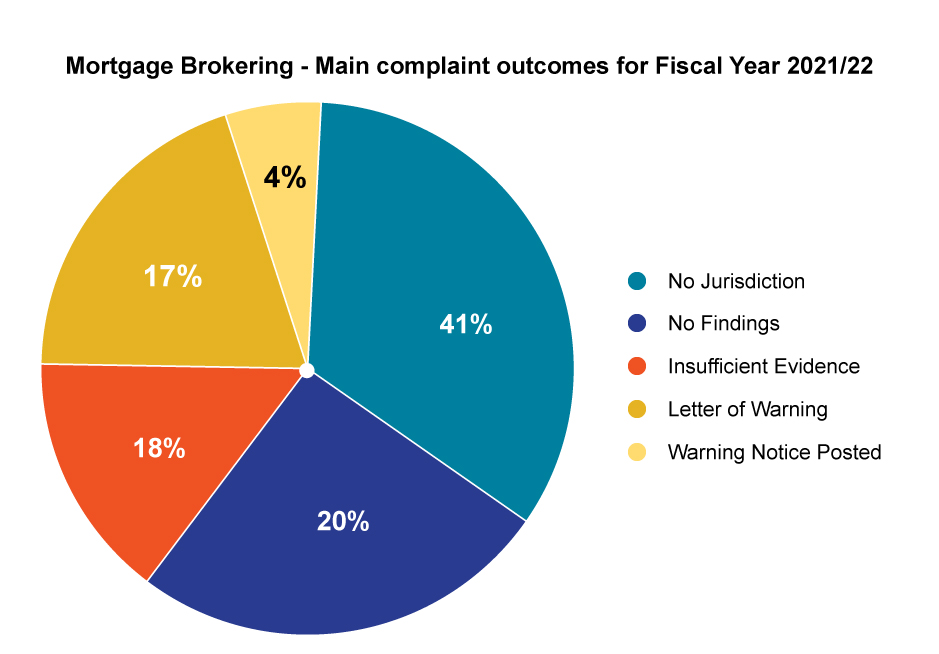

Although the highest number of complaints received are contractual in nature, they often carry the greatest consumer risk, including predatory lending and other practices targeted to take advantage of vulnerable individuals.

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. contractual matter | 22% |

| 2. unlicensed activity | 18% |

| 3. fraud/ illegal activity | 15% |

| 4. advertising | 12% |

| 5. customer service | 11% |

| 6. other* *other includes complaints regarding disclosure, suitability, administration, fees, policy/ procedures, etc. |

22% |

Image

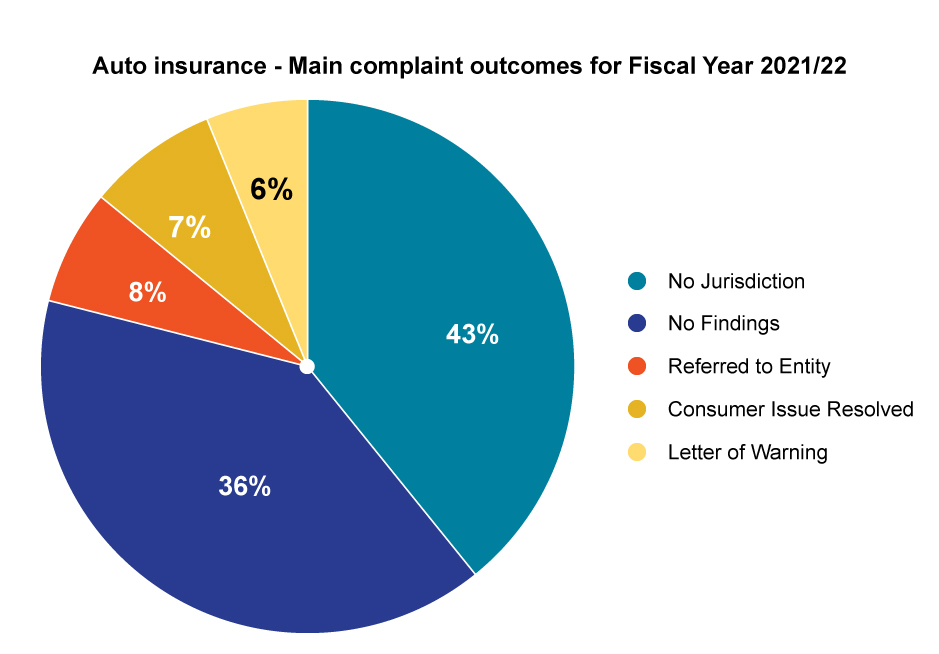

Auto insurance

FSRA is responsible for regulating auto insurance in Ontario. FSRA monitors the conduct of Insurers to ensure that they treat consumers fairly, comply with the Insurance Act and ensure that consumers are charged premiums based on auto insurance rates that FSRA has approved. Insurers are responsible for conducting themselves according to the regulatory regime, which includes Industry Codes of Conduct and FSRA Guidance. Examples include:

- conduct of Insurance Business and Fair Treatment of Customers

- Canadian Insurance Services Regulatory Organizations (CISRO) Principles of Conduct for Intermediaries

Insurers also need to comply with the Unfair or Deceptive Acts or Practices (UDAP) Rule, which came into effect on April 1, 2022, replacing the UDAP Regulation 7/00 under the Insurance Act.

Image

FSRA encourages insurers to assist the complainants in thoroughly understanding the claims process until resolution. If complainants are not satisfied, the insurers should provide alternate resolution options on whether to seek remediation through Civil Court, third-party dispute resolution bodies[1], or FSRA, if there are allegations of regulatory breaches.

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. claims and settlement | 42% |

| 2. customer service | 18% |

| 3. contractual matter | 14% |

| 4. premium calculation/ increase/ rebate | 7% |

| 5. policies and procedures | 4% |

| 6. other* *other includes complaints regarding administration, policy provisions, unlicensed activity, etc. |

15% |

Image

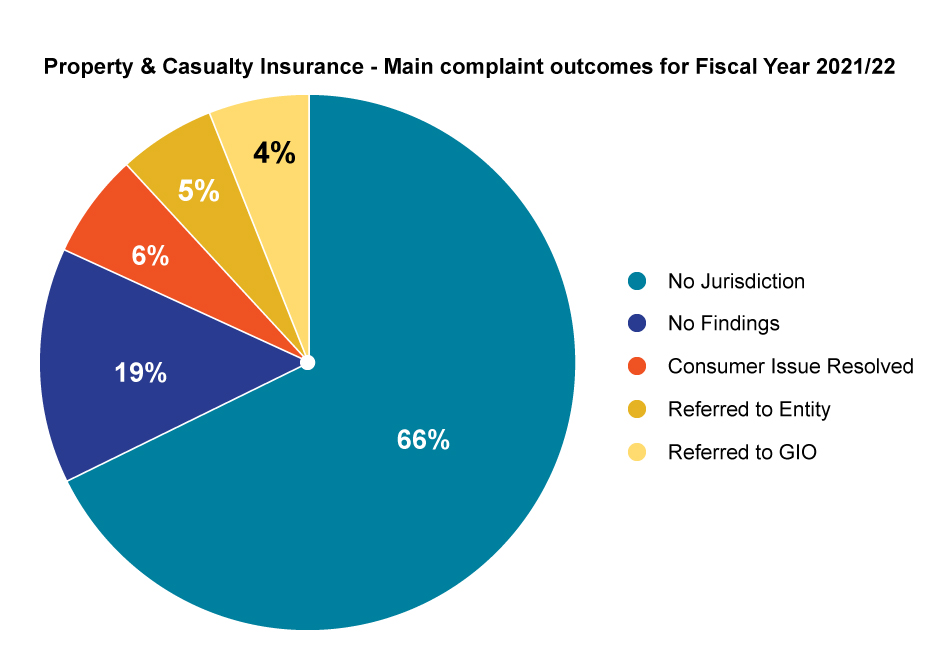

Property and casualty insurance

FSRA is the market conduct regulatory body for Ontario's property and casualty and general insurance sector. FSRA monitors the conduct of Insurers to ensure that they treat consumers fairly and comply with the Insurance Act. FSRA's role is also to ensure general agents comply with Ontario's laws, including meeting the qualifications and ongoing requirements for a license. FSRA also provides oversight to the independent and public adjusters and firms that investigate and advocate for claimants who have had other than auto insurance claims. Insurers are responsible for conducting themselves according to the regulatory regime, which includes these Industry Codes of Conduct and FSRA Guidance:

- conduct of Insurance Business and Fair Treatment of Customers Guidance

- Canadian Insurance Services Regulatory Organizations (CISRO) Principles of Conduct for Intermediaries

Insurers also need to comply with the Unfair or Deceptive Acts or Practices (UDAP) Rule, which came into effect on April 1, 2022, replacing the UDAP Regulation 7/00 under the Insurance Act.

Image

There was an increase in commercial insurance and condo/tenant insurance complaints. They were mostly related to the availability of insurance, premium increase, or non-renewals of policies. FSRA is working with the Ministry of Finance to understand industry practices and will engage with the insurance companies as necessary.

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. claims and settlement | 42% |

| 2. contractual matter | 18% |

| 3. customer service | 18% |

| 4. premium calculation/ increase/ rebate | 14% |

| 5. unlicensed activity | 2% |

| 6. other* *other includes complaints regarding adequacy of product, policy provisions, etc. |

6% |

Image

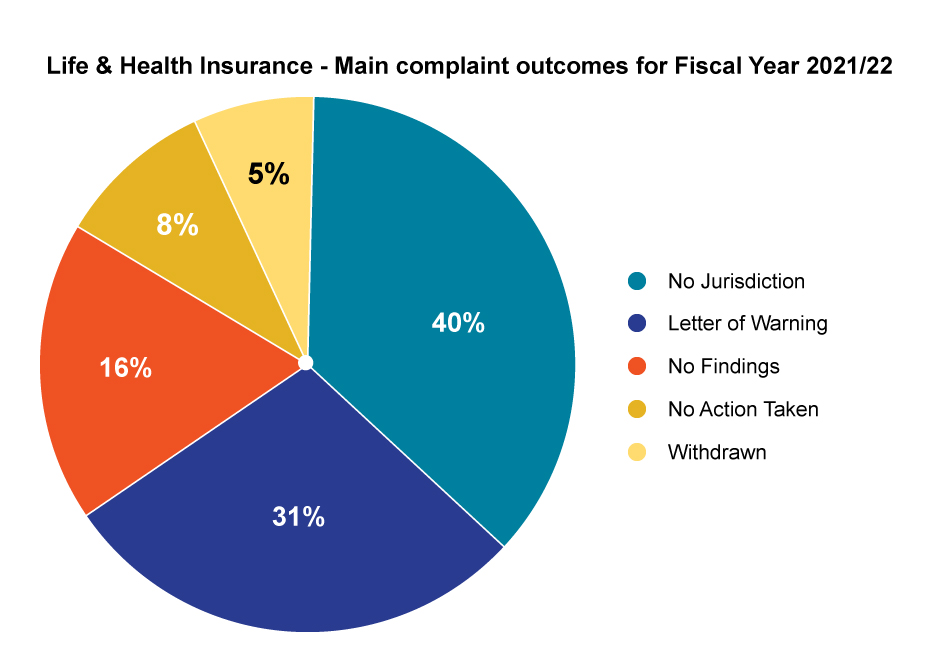

Life and health insurance

FSRA regulates Ontario's life and health insurance sector, including accident and sickness insurance. FSRA's role is to ensure agents and businesses that sell life and health insurance comply with Ontario's laws, including meeting the qualifications and requirements for a license. Insurers should be aware of their responsibilities outlined in these Industry Codes of Conduct and FSRA Guidance to ensure that they know their clients and sell suitable products:

- conduct of Insurance Business and Fair Treatment of Customers Guidance

- Canadian Insurance Services Regulatory Organizations (CISRO) Principles of Conduct for Intermediaries

- life agent reporting requirements and related insurer obligations

- CLHIA Guidelines

Insurers also need to comply with the Unfair or Deceptive Acts or Practices (UDAP) Rule, which came into effect on April 1, 2022, replacing the UDAP Regulation 7/00 under the Insurance Act.

Image

As part of our role to ensure high standards of business conduct, we conduct a scan of enforcement actions taken by other regulatory bodies. Should we find any of our licensees sanctioned under other legislation, we review the matter and may also take enforcement action as appropriate.

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. regulatory action in other jurisdictions | 28% |

| 2. claims and settlement | 14% |

| 3. contractual matter | 9% |

| 4. administration | 8% |

| 5. fraud/illegal activity | 7% |

| 6. other* *other includes complaints regarding customer service, policy provisions, advertising, premium increase, etc. |

34% |

Image

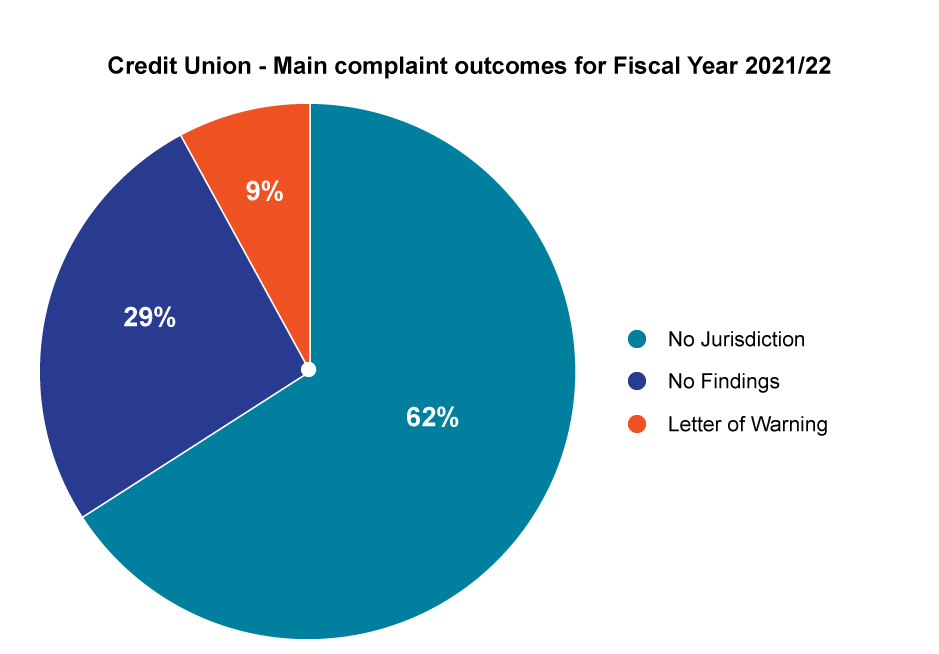

Credit unions and caisses populaires

FSRA regulates the credit unions and caisses populaires sector in Ontario. We protect Ontarians and strengthen the industry through deposit insurance and prudential oversight. Credit Unions are encouraged to formalize and document policies and procedures to avoid process-related complaints. Consumers expect formalized processes so that consistent application of internal policies may be carried out.

FSRA released the Market Conduct Framework Guidance that took effect on November 29, 2021. The Guidance outlines:

- FSRA’s interpretation of the existing Standards of Sound Business and Financial Practices (By-law No. 5) and section 102 of the newly proclaimed Credit Unions and Caisses Populaires Act, 2020

- FSRA’s approach to supervising and enforcing against market conduct frameworks adopted by credit unions

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. customer service | 20% |

| 2. disclosure | 18% |

| 3. contractual matter | 15% |

| 4. administration | 13% |

| 5. policies and procedures | 13% |

| 6. other* *other includes complaints regarding fees, fraud, advertising, etc. |

23% |

Image

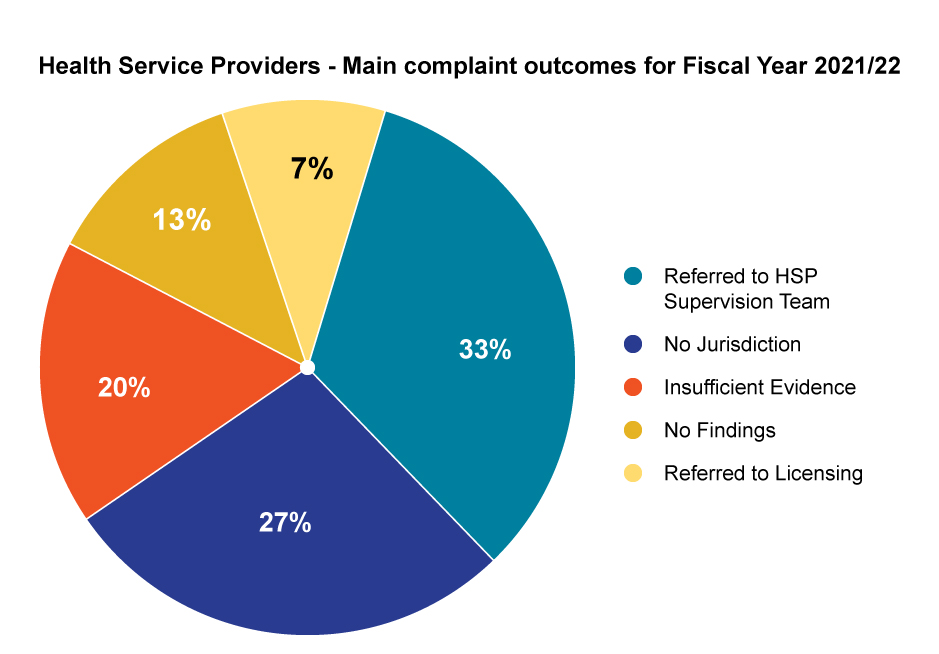

Health service providers

FSRA is responsible for oversight of the business operations of "Health Service Providers" engaged in providing goods and services to auto insurance accident benefits claimants. Health Service Providers are typically health and rehabilitation clinics and providers of assessments and examinations. FSRA's oversight of this sector specifically pertains to the business and billing practices of licensees with respect to auto insurance injury claims under the Statutory Accident Benefits Schedule (SABS).

To learn more about FSRA’s oversight of the health service providers, please see the Health Service Provider Market Conduct Compliance Annual Report that FSRA published in August 2022.

Image

The most common complaints in the HSP sector were related to the service provider's billing practices. In light of insufficient evidence, the CRAU team referred these complaints to our supervisory team to consider examination for these clinics.

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. administration | 40% |

| 2. fraud/illegal activity | 27% |

| 3. regulatory action in other jurisdictions | 13% |

| 4. policies and procedures | 13% |

| 5. contractual matter | 7% |

Image

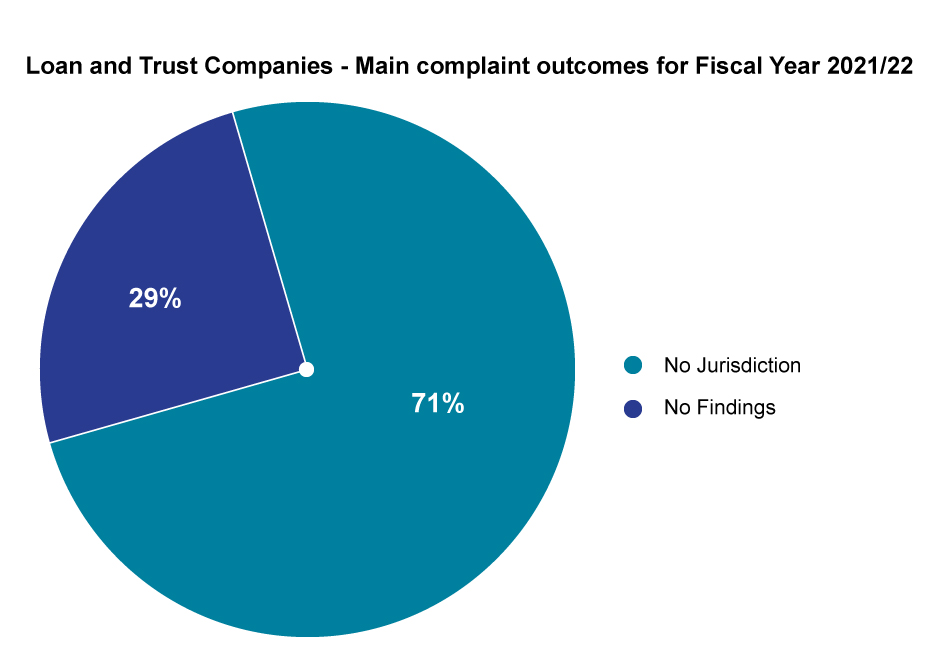

Loan and trust companies

FSRA registers all federally incorporated loan and trust companies that conduct business in Ontario and is responsible for market conduct oversight, including enforcing laws and regulations against unlicensed deposit-taking. All loan and trust companies must be federally incorporated with Canada's Office of the Superintendent of Financial Institutions (OSFI), the primary regulator for this sector.

Businesses undertaking deposit-taking or trust company activities servicing Ontario consumers must comply with the Loan and Trust Companies Act of Ontario (LATCA).

Image

FSRA received few complaints for this sector (10 this fiscal), most regarding contractual matters such as account terms. These matters fall outside our jurisdiction.

Complaint themes 2021/22

| Type of complaint | Amount in percentage |

|---|---|

| 1. contractual matter | 70% |

| 2. unlicensed activity | 30% |

Image

Appendix: FSRA service standards - complaints

| Sector (s) | Standard | Target % | Stretch target % |

|---|---|---|---|

| Life & Health, Auto and Property & Casualty Insurance, Health Service Providers, Mortgage Brokers, Credit Unions, Financial Planners and Financial Advisors, and Loan & Trust | FSRA will acknowledge complaints in writing within three business days of receipt, provided that the reply information is available. | 90% | 100% |

| Within 120 days, complaints containing all available information[3] will be assessed and actioned for various possible outcomes, including escalation to other areas of FSRA, transfer to third-party dispute bodies[1], warning letters, and closed with no action. | 80% | 85% | |

| Within 270 days, complaints containing all available information[2]will be assessed and actioned for various possible outcomes, including escalation to other areas of FSRA, transfer to third-party dispute resolution bodies[1], warning letters, and closed with no action. | 95% | 98% |

[1] The Pensions Department handles Pension Plan complaints and the statistics are not included within this report

[2] General Insurance Ombudservice (GIO) for P&C, Ombudservice for Life and Health Insurance (OLHI) for Life Companies

[3] Must include relevant facts and details, supporting documents and final position letter from subject entity.