Guidance

☑ Interpretation ☑ Approach ☐ Information ☐ Decision

No. PE0301INT Active

Purpose

The purpose of this Guidance is:

- To inform stakeholders of how FSRA interprets certain Pension Benefits Act (PBA) provisions relating to certain plan amendments which are determined to be Retroactive Adverse Amendments (as defined below)

- To describe FSRA’s approach to:

- Retroactive Adverse Amendments[1] including those purporting to rectify drafting errors in plan terms

- amendments that purport to replace a variable indexation formula with a fixed indexation rate for benefits already accrued

- notice requirement for certain adverse amendments

This Guidance is intended to protect plan beneficiaries, encourage timely filing of amendments and promote good plan administration, consistent with FSRA’s objects. It is not intended to address all questions or issues related to plan amendments and is limited to the interpretation and approach topics specifically listed above.

Scope

This Guidance applies to and affects the following entities regulated or registered by FSRA:

- pension plans[2]

This Guidance also affects the following stakeholders:

- pension plan beneficiaries[3]

- pension plan administrators

- sponsoring and participating employers

- collective bargaining agents

- third party advisors

Background

FSRA’s role under the PBA, having regard to its objects under the Financial Services Regulatory Authority of Ontario Act, 2016 (FSRA Act), is to enforce the standards set out under the PBA to:

- protect pension plan beneficiaries

- promote good administration of pension plans[4]

FSRA’s objects inform its[5] review of filed pension plan amendments. This includes FSRA’s exercise of discretion on whether to register an amendment[6] or refuse or revoke the registration of an amendment.[7]

Relevant statutory provisions[8]

This Guidance references sections 12 to 14 of the PBA as well as sections 18, 19 and 26, all of which are summarized in Appendix A. These provisions:

- establish registration requirements for pension plan amendments, including filing timelines

- describe amendments that are void under the PBA

- establish when FSRA can refuse or revoke registration of an amendment

- describe notice requirements for “adverse” amendments

Plan administrators should be familiar with PBA requirements relating to plan amendments they wish to file.[9] This includes filing timelines. Plan administrators must also ensure they satisfy the standard of care under section 22 of the PBA. This means acting prudently and with the required degree of care, diligence and skill when preparing and filing the amendment with FSRA.

Plan administrators have the obligation to ensure that plans, and amendments to a plan, are administered in accordance with all legislative requirements. Administrators should seek appropriate advice from external service providers, where necessary, to ensure they satisfy their obligations.

Retaining appropriate records relating to plan amendments is important. Administrators may want to review FSRA’s Pension Plan Administrator Roles and Responsibilities Guidance regarding their records retention responsibilities.

Interpretation

Amendments with retroactive adverse effects

This section applies to both defined benefit and defined contribution pension plans.

Retroactive Adverse Amendments are generally not permissible

In certain cases, plan administrators may seek to register amendments which:

- may negatively impact members’ or beneficiaries’ rights and/or benefits

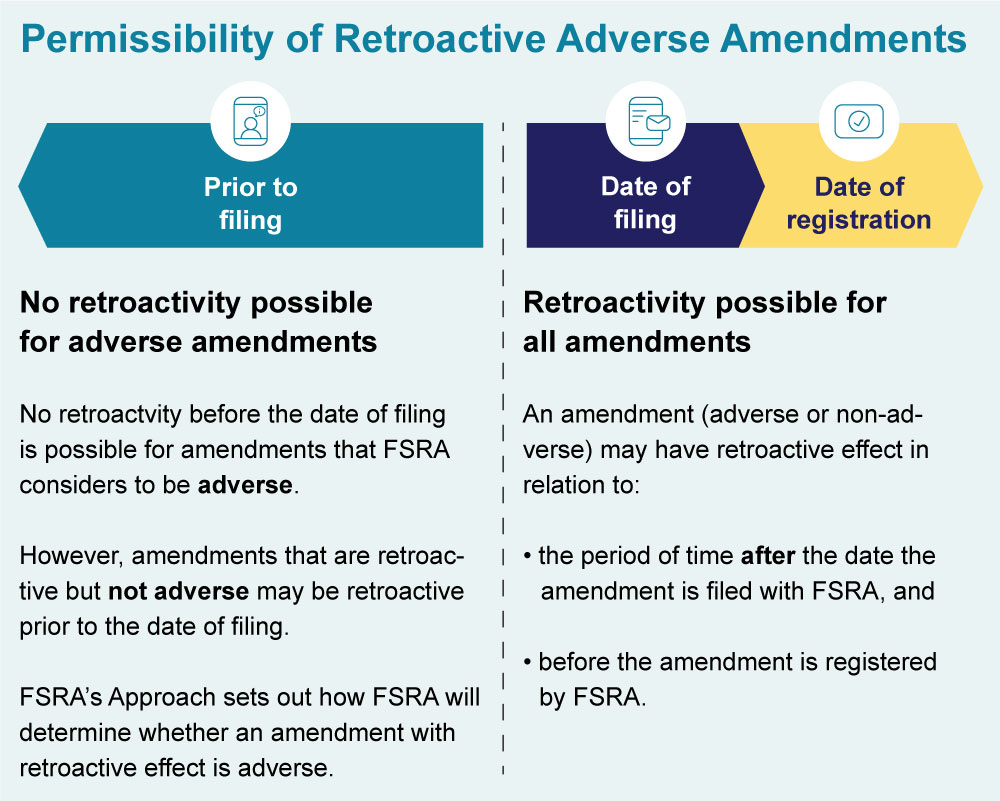

- purport to be effective on a date before the amendment is filed with FSRA

FSRA generally considers these to be “Retroactive Adverse Amendments”. FSRA’s Interpretation is that the PBA generally does not permit Retroactive Adverse Amendments.[10] See Appendix A for FSRA’s full analysis of the relevant provisions.

In considering amendments, FSRA must make an initial determination as to whether a proposed amendment, or any part thereof, will contravene the requirements of the PBA. In doing so, FSRA must consider the provisions of the PBA and the impact of an amendment having regard to its statutory objects under the FSRA Act referenced above.

As part of that analysis of whether an amendment contravenes the PBA, FSRA must interpret the PBA as being “remedial and afford it a fair large and liberal interpretation as best ensures that attainment of its objects.”[11] This broader statutory context supports the view that Retroactive Adverse Amendments are not permitted under the PBA based on the general proposition that statutory provisions are presumed to not permit the interference with the rights of individuals, who in this case are plan members, with retroactive adverse effect.[12] FSRA has discretion under section 18 of the PBA to refuse to register an amendment that interferes with an existing benefit or status such that it would constitute a Retroactive Adverse Amendment, and as a result not comply with the requirements of the PBA.[13]

Determining if the amendment is a Retroactive Adverse Amendment

Whether an amendment qualifies as a Retroactive Adverse Amendment is determined by whether the amendment truly has an “adverse effect.” FSRA determines this by considering the totality of the nature and effect of the amendment on the rights and benefits of the beneficiaries, as well as the PBA provisions relevant to the amendment.

In some cases, it may be obvious a plan amendment has an adverse effect and is therefore not permitted under the PBA. This may be the case, for example, where the amendment is retroactive prior to the date of filing, and the amendment:[14]

- increases member contributions to a defined benefit pension plan

- reduces accruals in a defined benefit pension plan

- removes portability rights for plan members who have reached early retirement age under the plan terms

Some of these amendments may also be void under section 14 of the PBA.

However, it is possible for an amendment to have a retroactive impact on rights and benefits and not be considered a Retroactive Adverse Amendment. This is the case where the amendment does not truly have an “adverse effect”. This can only be determined after considering:

- the circumstances of the amendment

- the text, context, and purpose of the PBA provisions at issue

- the broader purpose of the PBA

- whether the exercise of FSRA’s discretion to register the amendment would be consistent with FSRA’s statutory objects

Where an amendment purports to be retroactive prior to the date of filing with FSRA, the administrator must demonstrate to FSRA it is appropriate to register such an amendment on the basis it that does not have an “adverse effect”. FSRA will generally exercise its discretion and register such an amendment where the plan administrator is able to demonstrate both of the following:

- the negative retroactive impacts on the rights and benefits of plan members and beneficiaries are non-material

- These impacts are offset by considerations of transparency, reasonableness and equity.[15]

Examples where this may occur include, but are not limited to, the following situations:

- An amendment has a negative retroactive impact (e.g., increases in member contribution rates prior to date of filing). However, the employer and union have negotiated the change as part of collective bargaining and the amendment supports the terms of a collective agreement.

- An amendment such as the one described by the majority of the Supreme Court of Canada in Nolan v. Kerry (Canada) Inc..[16] This is limited to the specific, or equivalent, fact situation in that case.[17]

- In certain cases, amendments that support corporate reorganizations. For example, where changes have clearly been communicated to beneficiaries and the delay in filing is reasonable.

In addition to the above examples, retroactive amendments that do not have any adverse impact on member benefits and entitlements are not Retroactive Adverse Amendments. These include:

- retroactive amendments that provide benefit improvements

- retroactive amendments that change plan terms to comply with PBA or other applicable legislative requirements

Approach

Amendments with retroactive adverse effects

This section applies to both defined benefit and defined contribution pension plans.[18]

A plan administrator may apply to FSRA for registration of an amendment that has retroactive negative impacts. The administrator must demonstrate a reasonable and good faith belief the amendment is not a Retroactive Adverse Amendment. When applying for registration, the administrator should, in its application:

- identify that the amendment has retroactive negative impacts, or

- identify that the administrator nevertheless does not believe it qualifies as a Retroactive Adverse Amendment

Administrators are encouraged to discuss such amendments with FSRA before filing. They should also be prepared to make submissions addressing the registrability of the amendment that address competing arguments and are encouraged to provide a legal opinion to FSRA (separate from any opinions provided to the plan sponsor and/or administrator) that supports registration of the amendment. This will assist in expediting FSRA’s review. The submissions should outline any relevant factors that support the view that the amendment is consistent with the PBA. As with any instance of possible statutory non-compliance, FSRA’s determination will be specific to the facts under consideration.

Consistent with its statutory objects, as a principles-based and outcomes focused regulator, FSRA’s approach to evaluating and exercising discretion to register an amendment with retroactive and potentially negative impacts will be guided by considerations of transparency, reasonableness and equity. These include:

- Transparency:

Has the proposed amendment been communicated to plan members, beneficiaries, and impacted unions prior to filing with FSRA? Have concerns been raised with respect to the impact of the amendment. If so, how have they been addressed?

- The impact of the amendment:

What is the actual impact of the proposed amendment? Does it negatively impact the rights and benefits of members and plan beneficiaries? What is the scope of that impact?

- The reasons for the retroactive filing:

Was the failure to follow the filing process under the PBA reasonable in the circumstances? If the failure to file in a timely manner with FSRA was a result of inadvertence? What length of time elapsed between the purported effective date and the date of filing? Was the delay reasonable in the circumstances?

- Is the amendment equitable:

Does the amendment treat plan members and beneficiaries, and their rights and entitlements, in a fair and equitable manner? FSRA recognizes employers, plan administrators and members sometimes face difficult choices about the sustainability of the plan. Those difficult choices may require retroactive solutions to achieve fairness between different groups of members.

FSRA will also consider whether the filing of the amendment would be consistent with the administrator’s fiduciary duty as it relates to their obligations with respect to amendment filings under the PBA. Administrators should address in their submissions to FSRA how, in filing the amendment for registration, the administrator has been able to attest that the amendment complies with the PBA and its associated regulations, as is required of the administrator under clause 12(2)(b.1) of the PBA.

In addition, to support the supervisory outcomes of:

- transparency

- predictability

- effective plan administration

- consistent treatment of similar applications

FSRA will publish details of amendments FSRA has determined do not meet the definition of a Retroactive Adverse Amendment. In doing so, FSRA will not refer to the identity of the plan or its administrator. FSRA will determine, based on the circumstances, the level of detail to be published. FSRA will not disclose competitive or sensitive information related to a plan or the administrator.

Finally, administrators should be aware that section 13(2) of the PBA does not permit an administrator to cure any prior non-compliance with the existing plan terms or the PBA by filing a “retroactive” amendment. Section 19 of the PBA requires an administrator to ensure that the pension plan and pension fund are administered in accordance with the PBA, regulations, FSRA rules and filed documents. An administrator cannot cure any non-compliance with that responsibility by a retroactive amendment.

Retroactive amendments purporting to rectify drafting errors in the plan terms

FSRA does not have authority under the PBA to rectify drafting errors by registering a Retroactive Adverse Amendment. Rectification of a pension plan’s terms is within the jurisdiction of the Ontario Superior Court of Justice. FSRA may, in its discretion, support a court application by an employer or plan administrator for rectification.[19]

Replacing a variable indexation formula with a fixed rate (accrued benefits)

An amendment is void under section 14 of the PBA if it purports to reduce the amount or value of certain benefits already accrued under the pension plan.

FSRA has received applications for registration of plan amendments that, with respect to benefits already accrued, purport to:

- remove a variable indexation formula, or

- replace that formula with a fixed indexation rate

These amendments are generally considered by FSRA to be void under section 14. This is because they have the potential to reduce the amount or commuted value of accrued benefits. This is the case whether or not the fixed indexation rate currently exceeds, or is thought likely to exceed in the future, the rate determined by the formula.

It may be possible for an indexation formula to be amended without violating subsection 14(1) of the PBA.[20] For example, the variable rate formula could be maintained as a floor to a fixed rate. In this case, the beneficiary would receive the greater of the fixed or variable rate. The amendment would therefore not be considered by FSRA to be void. Administrators are encouraged to discuss any special circumstances that may exist, such as on plan wind up, with FSRA.

This position is subject to the exceptions set out in section 14 of the PBA.

Notice requirements for prospective adverse amendments

Section 26 of the PBA establishes notice requirements for plan amendments that:

- reduce subsequently accrued pension benefits, or

- “would otherwise adversely affect the rights or obligations” of beneficiaries

FSRA requires administrators to transmit notice to persons affected by such amendments as described under section 26. As described under section 26, there is a 45 day period after the date of providing notice before FSRA may register the amendment.

Subsection 26(4) of the PBA gives FSRA discretion to dispense with this notice requirement in the circumstances described in clauses (a) to (c). An administrator can request in writing that FSRA exercise its discretion to not require notice. Such a request should indicate which circumstances the administrator believes apply. Administrators should not assume FSRA has, or will, waive notice requirements simply because they believe a circumstance applies.

If an administrator files an “adverse” amendment but:

- does not transmit a notice pursuant to subsection 26(1), or

- does not obtain a waiver pursuant to subsection 26(4)

it is possible FSRA will later determine that the amendment is “adverse.” In this case, FSRA may require the administrator to transmit a notice at that time. This is regardless of whether a certificate of registration has already been issued for the amendment. General administrative penalties may also be applied as described in the “Penalties” section of this Guidance.

A notice pursuant to subsection 26(1):

- Does not need to contain the word “adverse.” However, it must provide an appropriate description or explanation of the amendment.

- Must indicate that questions or comments about the amendment can be provided to the administrator or FSRA.

- Does not affect the filing of the related amendment. In other words, there is no need to delay filing the amendment until after the notice period.

- Does not remedy an otherwise void or non-compliant amendment. It also does not cure non-compliance with the plan terms as they existed before the amendment.

FSRA reminds administrators of their obligation to communicate clearly to beneficiaries any changes to the plan. This is set out in FSRA’s Pension Plan Administrator Roles and Responsibilities Guidance.

Notice of Intended Decision to refuse to register an amendment to a plan

FSRA may refuse to register an amendment to a pension plan, or part of an amendment to a pension plan. If so, FSRA is required to serve on the applicant or administrator of the plan:

- a notice of the intended decision (NOID); together with

- written reasons for the intended decision[21]

The NOID must state the person served is entitled to a hearing by the Financial Services Tribunal (FST). This depends on the person delivering written notice requiring a hearing to the FST within thirty days of receipt. Where a written request is not made in time, FSRA may make the intended decision in the NOID.

Penalties

FSRA may levy general administrative penalties of up to $25,000 against an administrator that fails to comply with subsections 12(1), 19(3) or 26(5)[22]of the PBA.[23]Failure to comply with the PBA, its regulations or a FSRA Rule is also an offence under the PBA. An offence can be subject to penalties under the PBA. These include fines of up to:

- $100,000 for the first offence

- $200,000 for subsequent offences[24]

FSRA is a principles-based and outcomes-focused regulator.[25] This means FSRA takes a progressive, measured, and proportional approach to enforcement. Where a plan administrator has not complied with requirements, FSRA will determine the appropriate action after considering the evidence and circumstances at issue. This includes:

- the seriousness and nature of the contravention

- the risk presented to plan beneficiaries

- past behaviour

- efforts to remediate and mitigate

- the need for deterrence

FSRA will strive to be measured in its approach to compliance and enforcement. FSRA assumes good faith by the plan administrator and will be measured and proportional in its approach to enforcement of the PBA.

Effective date and future review

This Guidance becomes effective on June 4, 2024 and will be reviewed no later than June 4, 2029.

About this Guidance

This document is consistent with FSRA’s Guidance Framework. As Interpretation Guidance, it describes FSRA’s view of requirements under its legislative mandate (i.e., legislation, regulations, and rules) so that non-compliance can lead to enforcement or supervisory action. As an Approach, it describes FSRA’s internal principles, processes and practices for supervisory action and application of FSRA’s discretion.

Appendix A

Summary of relevant PBA provisions

Subsection 19(3) requires the administrator of a pension plan ensure the pension plan and pension fund are administered in accordance with the plan documents filed with FSRA.

Subsection 19(5) permits administration in accordance with an amendment to the plan where an application to register the amendment with FSRA has been made and registration or refusal of registration is pending. However, administration in accordance with an amendment is permitted only if:

- the application complies with the PBA and its regulations

- and the amendment is not void under the PBA

Section 12 requires the plan administrator to apply to FRSA to register any amendment that has been made to the plan, within 60 days of the amendment. It also requires the administrator to certify that the amendment complies with the PBA and its regulations. Registration of the amendment is not an “approval” by FSRA. It should not be taken as a confirmation by FSRA that the amendment is compliant with the PBA.

Subsection 13(1) provides that an amendment to a pension plan is not effective until the plan administrator files an application with FSRA for registration of the amendment that meets the requirements of section 12. However, subsection 13(2) provides that an amendment may be effective before the date the amendment is registered by FSRA.

Subsection 14(1) describes amendments that are void under the PBA. An amendment to a pension plan is void if the amendment purports to reduce the amount or commuted value of a pension benefit accrued by a pension plan beneficiary under the plan. Any reduction of the amount or commuted value of an ancillary benefit where a plan beneficiary has already met all eligibility requirements under the plan terms is also void. Subsections 14(2) to (7), meanwhile, provide exceptions to the void amendment prohibition in subsection 14(1) for certain kinds of pension plans and plan transactions.

Section 18 provides that the registration of non-compliant amendments can be refused or revoked by FSRA. The onus is on employers and plan administrators to ensure compliance with the PBA. Registration of an amendment does not relieve an administrator of the duty to comply with the requirements of the PBA.

Section 26 requires the plan administrator to provide notice of plan amendments to the plan’s members and other beneficiaries, and particularly notice of “adverse” amendments (i.e., amendments that reduce pension benefits accruing after the effective date of the amendment or that would otherwise adversely affect the rights or obligations of any plan beneficiaries). Subsection 26(2) provides that FSRA shall not register an adverse amendment until 45 days after the administrator has given notice of the adverse amendment.

FSRA’s statutory interpretation relating to Retroactive Adverse Amendments

FSRA’s interpretation of the relevant provisions of the PBA is consistent with a broad and purposive approach to statutory interpretation.

This requires that the “interpretation of a statutory provision must be made according to a textual, contextual and purposive analysis to find a meaning that is harmonious with the Act as a whole.” [26] It also requires that “the words of an Act are to be read in their entire context and in their grammatical and ordinary sense harmoniously with the scheme of the Act, the object of the Act, and the intention of Parliament.”[27]

This approach to statutory interpretation has been codified in section 64 of the Legislation Act, 2006. That Act requires that every statute in Ontario, including the PBA, “shall be interpreted as being remedial and shall be given such fair, large and liberal interpretation as best ensures the attainment of its objects.”

Consistent with this approach, and with respect to amendments that purport to have retroactive negative impacts, FSRA interprets the requirements of subsections 19(3), 13(1) and 13(2) of the PBA in the following manner:

- Subsection 19(3) of the PBA requires that the administrator of a pension plan ensure that the pension plan and pension fund are administered in accordance with the plan documents filed with FSRA. Subsection 13(1) of the PBA provides that an amendment to a pension plan is not effective until the plan administrator files an application with FRSA for registration of the amendment that meets the requirements of section 12.

As a result, FSRA’s view is that until the date a plan amendment is filed with FSRA for registration, the terms of the plan, as they exist before the date the amendment is filed, still apply to the plan benefits and the plan administrator’s obligations. - Subsection 13(2) of the PBA provides that a pension plan amendment may be made effective as of a date before the date on which it is registered by FSRA. However, this does not mean that an amendment is permitted to have a retroactive adverse effect on the plan’s beneficiaries. In FSRA’s view, a clear expression of legislative intent is required for legislation to have retroactive effect,[28] particularly where retroactivity would interfere with vested rights (such as pension entitlements granted under the terms of a pension plan). Therefore, it is FSRA’s interpretation that subsection 13(2) does not, read alone or with subsection 13(1), express a clear legislative intent that amendments be permitted to have adverse retroactive effects.

- Subsections 13(1) and 13(2), when read together, suggest that a retroactive amendment can become effective on the date before the amendment is registered with FSRA for registration, while also recognizing that the registration of the amendment by FSRA may, in practice, occur sometime after the amendment’s filing date. Subsection 13(2) therefore permits the retroactive effect of an amendment to be applied by the plan administrator from the date the amendment is filed with FSRA, even though the registration of the amendment by FSRA could occur sometime after the date of filing.

A textual and contextual reading of subsections 19(3), 13(1) and 13(2) supports the conclusion that these provisions operate to protect plan members from the potential negative effects of any administrative delay between the filing of an amendment with FSRA and the registration of that amendment by FSRA.

When applying the various sections of the PBA related to plan amendments, section 13(2) does not change the general approach under the PBA that amendments that have an adverse impact on plan beneficiaries be made prospectively. On this basis, FSRA interprets subsection 13(2) as permitting a plan amendment to have retroactive effects only in relation to the period of time after the date the amendment is filed with FSRA for registration and before the amendment is registered by FSRA. However, if an amendment is retroactive prior to the date it is filed with FSRA but not considered to be an Adverse Retroactive Amendment, FSRA will generally exercise its discretion and register it.

In FSRA’s view, subsection 13(2) prevents the registration requirement under the PBA from potentially negatively affecting plan beneficiaries by allowing an amendment to take effect once it is filed, even though the registration of the amendment by FSRA may occur at a later date. Operating in that way, subsection 13(2) is thus consistent with the object and purpose of the PBA and the applicable statutory objects under the FSRA Act.

When the relevant provisions related to plan amendments are read in their whole context and with a view to ascertaining their purpose, it can be said that a key goal of the PBA is to prevent reductions in benefits in a manner that is unfair or inequitable to plan beneficiaries. Amendments that interfere with accrued benefits are void pursuant to section 14. Amendments that will have adverse effects, even on a prospective basis, are subject to a special notice and comment procedure under section 26, and are permissible only in specified circumstances. Had the legislature intended the PBA to allow retroactive adverse changes to the rights of plan beneficiaries, this would have been explicitly stated in the PBA.

Effective date: June 4, 2024

[1] “Retroactive Adverse Amendment” is not a defined term in the PBA. It is used in this Guidance as a description for the type of amendments described under the section “Amendments with Retroactive Adverse Effects”.

[2] The scope of this Guidance includes all pension plans within FSRA’s jurisdiction, including multi-employer pension plans (MEPPs) which are subject to specific requirements prescribed under the PBA with respect to amendments. Therefore, the application of this guidance to MEPPs will be modified as necessary, noting that MEPPs have broad authority to amend their plans, including the ability to reduce the amount or commuted value of benefits pursuant to section 14 of the PBA.

[3] In this Guidance, a pension plan’s beneficiaries include the plan’s members, former members, retired members and other beneficiaries entitled to payments from the plan.

[4] See subsection 3(3) of the FSRA Act.

[5] Under the provisions of the PBA, the CEO is granted regulatory authority to refuse to register an amendment to a pension plan if the amendment is void or the pension plan with the amendment would cease to comply with the PBA and its regulations. For purposes of this Guidance, references will be to FSRA, as the CEO delegates this power within FSRA as permitted by subsection 10(2.3) of the FSRA Act.

[6] Pursuant to section 12 of the PBA

[7] Pursuant to section 18 of the PBA

[8] Please refer to the actual PBA provisions cited for details of each of the requirements described in this Guidance, including the Appendix.

[9] Please refer to FSRA’s Pension Plan Administrator Roles and Responsibilities Guidance.

[10] FSRA notes that subsection 14(2) of the PBA permits MEPPs to reduce the amount or commuted value of accrued benefits. Nothing in this Guidance is intended to affect or restrict such benefit reductions.

[11] See subsection 64(1) of the Legislation Act, 2006, S.O. 2006, c. 21, Sched. F. See also Monsanto Canada Inc. v. Ontario (Superintendent of Financial Services), [2004] 3 S.C.R. 152, 2004 SCC 54 where the Court noted that “the Pensions Benefits Act is clearly public policy legislation establishing a carefully calibrated legislative and regulatory scheme prescribing minimum standards for all pension plans in Ontario. It is intended to benefit and protect the interests of members and former members of pensions plans.”

[12] See Brown, Donald J. M. and Evans, J. M., "Judicial Review of Administrative Action in Canada" (1998).

[13] See Brewers Retail Inc. v. Campbell, 2023 ONCA 534 at para. 75 where the Court of Appeal noted that FSRA has authority to refuse to register an amendment which it had determined to be adverse and the plan administrator would only be able to address that through seeking a hearing before the Financial Services Tribunal

[14] This list is not intended to be exhaustive.

[15] See the Approach section of this Guidance for a description as to how FSRA will exercise its discretion.

[16] Nolan v. Kerry (Canada) Inc., 2009 SCC 39

[17] In the Nolan v. Kerry (Canada) Inc. case, the employer’s intention to implement the effect of what would eventually be a retroactive plan amendment was known to all parties from the time that effect was intended to apply, and was the subject of litigation between the parties from that time onwards. When that litigation reached the Supreme Court of Canada, the majority of the Court determined that a retroactive amendment to implement the employer’s intended effect back to the employer’s intended implementation date would not, in the particular circumstances of the plan and the amendment, affect any plan beneficiary’s vested rights under the plan, and the retroactive amendment was permitted under the PBA.

[18] The approach in this section does not apply to an amendment to a MEPP which reduces benefits pursuant to subsection 14(2) of the PBA.

[19] FSRA will determine whether or not to support an application to court for rectification based on its consideration of the basis for the relief sought.

[20] See McGrath v. Ontario (Superintendent Financial Services), 2010 ONFST 5, wherein the Financial Services Tribunal noted that the crucial question is whether a proposed amendment reduces the amount or commuted value of the plan member’s pension, meaning whether it on its face does so or has the effect of doing so based on the information available at the time the amendment was adopted by the plan sponsor.

[21] See subsection 89(1) of the PBA.

[22] This is a non-exhaustive list citing only the provisions that are relevant to this Guidance. FSRA may levy general administrative penalties with respect to a number of other sections of the PBA.

[23] See section 108.2 of the PBA, in conjunction with Ontario Regulation 365/17 (Administrative Penalties).

[24] See section 110 of the PBA.

[25] Please refer to FSRA’s Proposed Principles-Based Regulation Approach Guidance.

[26] Canada Trustco Mortgage Co. v. Canada, 2005 SCC 54 at paragraph 10.

[27] Rizzo & Rizzo Shoes Ltd. (Re), [1998] 1 SCR 27 at paragraph 21.

[28] See Ruth Sullivan, Construction of Statutes (7th ed. 2022), at para. 25.