Executive summary

Consumers looking to obtain or invest in a mortgage are facing greater risks due to rising interest rates, higher inflation and a volatile housing market. These factors increase the need for regulators to supervise the mortgage brokering sector, especially with respect to how mortgage brokerages and administrators provide services and products to more financially vulnerable clients.

FSRA’s 2023-24 Mortgage Brokering Sector Supervision Plan builds on the progress we have made in the past to make sure brokerages, brokers, agents and administrators are protecting clients and keeping clients’ interests top of mind. This plan is intended to achieve the following outcomes by ensuring:

- Consumers receive mortgage recommendations that are suitable for their needs and circumstances

- Investors and lenders have confidence that mortgage administrators are protecting the investments and funds in their care.

As a result, FSRA has identified the following supervision areas of focus for 2023-24. This includes reviewing:

- Brokerages’ practices to ensure private mortgages are suitable for consumers and consumers understand the product features and costs, including consideration of an exit strategy

- The conduct culture, compliance structure and principal broker’s supervision in large brokerages to ensure all brokers and agents are conducting their activities with integrity and competence

- Practices of licensed administrators, brokerages and/or their related parties who provide services to investors during the life cycle of a mortgage investment.

In addition, FSRA will finalize its proposed Guidance on Mortgage Administrator’s Financial Filing Requirements. The proposed Guidance will clarify existing reporting requirements and expand the scope of the required audit on compliance with specific MBLAA requirements. The objective is to protect funds and investments mortgage administrators handle for investors.

FSRA will also issue guidance on mortgage suitability to further clarify our expectations on how the sector can demonstrate that the mortgage recommendations they present to clients are suitable based on the client’s needs and circumstances.

FSRA is also expanding our education content on private mortgages to support consumers who need to turn to private mortgages to finance their homes.

Background

A FSRA consumer survey from January 2023 indicates about half of Ontario consumers use mortgage brokers to obtain their mortgages. Financially vulnerable respondents are more likely to use a mortgage broker.[1] Amid reduced mortgage affordability and high debt it is crucial the sector recommends suitable products and services for their clients’ needs and circumstances.

As of March 31, 2023, FSRA licensed 2,881 mortgage brokers and 14,005 mortgage agents with 1,231 brokerages. This compares to 2,833 brokers and 12,277 agents on June 30, 2019, representing nearly 12 percent growth between 2019 and 2023.

License holders brokered about 341,000 mortgages worth more than $193 billion in Ontario in 2022.[2]

As of March 31, 2023, FRSA licensed 242 mortgage administrators who administered about $350B and over 850,000 mortgage investments for 38,000 investors.

How does FSRA protect mortgage brokering consumers?

FSRA supervises and examines the business practices of mortgage brokerages, administrators, brokers and agents to ensure they:

- Provide products and services that are suitable for each client’s needs and circumstances;

- Help clients understand the features, risks and costs of their mortgages or mortgage investments;

- Provide services in a transparent and diligent manner; and

- Comply with all regulatory expectations and applicable legal and regulatory requirements.

Brokers and agents should keep their clients’ interests top of mind when providing mortgage advice. Consumers should ask questions if there is something they don’t understand.

FSRA’s 2022-2023 supervision focus and findings

FSRA focused its 2022-2023 supervision activities on brokering practices relating to private mortgages, mortgages from a related mortgage investment corporation (MIC) and reverse mortgages. Last year’s examinations revealed the following shortcomings:

- Brokers and agents did not retain documentation on why a mortgage recommendation is suitable for consumers;

- The annual percentage rate of borrowing is often understated;

- Conflicts of interest are not properly disclosed.

2022-2023 Year in review

What did we do?

The Bank of Canada (BOC) started raising its policy interest rate, which was at 0.25% in March 2022, to cool the economy and reduce inflation. It raised the rate to 5% on July 12, 2023,[3] a 20-fold increase in 16 months. During the same period, real estate corrections were also observed in some markets. Therefore, FSRA expected more consumers to turn to private mortgages because of higher rates. As a result, FSRA determined that private mortgage brokering remained a supervision focus for 2022-2023.

In addition, we observed the following trends and developments which could increase consumer protection risks in this sector:

- An increase in the number of new licensed brokers and agents who may have less experience, especially with providing advice and guidance to clients amid rising rates and higher inflation.

- Higher-than-average financial vulnerability of consumers in the mortgage brokering sector.[4]

These trends increase the risk that consumers are presented with unsuitable mortgage recommendations, or do not understand the features and implications of their mortgage. To address these concerns, FSRA identified the following supervision areas of focus for 2022-23:

- Continued focus on ensuring private mortgages are suitable for and are understood by borrowers.

- Review conduct culture, compliance structure and principal brokers’ supervision at large brokerages.

- Conduct supervisory research and compliance reviews in scenarios where financially vulnerable consumers may be at higher risk of misconduct or abuse.

In addition, with the new non-qualified syndicated mortgage investment (NQSMI) regime implemented in July 2021, FSRA examined how mortgage brokerages who broker NQSMI transactions are ensuring they only deal with permitted clients unless they have the appropriate securities registration. In addition, FSRA continued its review of mortgage administrators’ practices related to investments and funds handling, mortgage performance monitoring and reporting to investors.

|

|

Key Risks |

Supervision Focus |

|---|---|---|

|

Uncertainty because of rising interest rates, inflation and correction of housing prices in certain markets: difficulty for consumers to service their debts and access financing |

Continue to examine private mortgage brokering to ensure:

|

|

|

More licence holders with less experience, many of whom might not have experienced an inflationary market: inability to provide appropriate mortgage advice to consumers |

Examine conduct culture, compliance structure and principal brokers’ supervision at large brokerages to ensure:

|

|

|

Higher financial vulnerability of consumers in the mortgage brokering sector: they may be more exposed to misconduct or abuse |

Arranging mortgages for borrowers by brokerages who also manage a Mortgage Investment Corporation (MIC), to assess:

Brokering of reverse mortgages to understand this market and brokerages’ promotion and sales practices, including suitability assessment. |

Findings

We noted common issues when we examined industry practices in brokering mortgages for clients across the board:

- Unclear rationale for how a recommended mortgage is suitable for a client based on the client’s specific needs and circumstances. This lack of clarity does not allow clients to hold their brokers or agents accountable; principal brokers cannot properly oversee delivery of mortgage advice; and brokers and agents cannot prove the reasonableness of their recommendation.

- This observation was prevalent in all our examinations on brokering practices regarding private mortgages and mortgages from related MICs. A total of 68% of transactions reviewed for suitability rationale did not have documentation on why the mortgage recommendations were suitable.[5]

- Incorrect costs of borrowing, which at times were substantially understated and did not present the “true” cost of borrowing

- The annual percentage rate (APR) of borrowing incorporates the stated rate of a mortgage plus other costs incurred to obtain the mortgage. It provides borrowers with the “true” cost of borrowing. The calculation is prescribed in O. Reg. 191/08. FSRA noted in many cases the APR was understated. For example, in our review of mortgages from related MICs, 54% (37 of 69) had inaccurate APRs disclosed to the borrower. Similar findings were noted in our private mortgage brokering exams and reverse mortgage exams.

- Inadequate disclosure of conflicts of interest leading to clients incorrectly assuming they are receiving impartial mortgage recommendations from their brokerages

- We noted circumstances when a brokerage cannot be impartial to act in a client’s interest because the brokerage is either the lender or is related to the lender in a mortgage transaction. Disclosing such relationships helps borrowers consciously choose whether to continue working with the brokerage, or to bring in their own representation. However, FSRA observed inadequate disclosure of relationships resulting in real or potential conflicts of interest, for example, in our exams of brokering mortgages from private lenders and MICs that are related to the brokerage.

These findings raise consumer protection concerns, especially when private mortgages are involved. This is because private mortgages are often less standardized and more costly. Borrowers who must rely on them to finance their home purchase are often less financially resilient and literate. Consumers in these situations are, therefore, more prone to unfair treatment.

To ensure consumers receive suitable mortgage recommendations especially with private mortgages, FSRA is working with the MBRCC on harmonized mortgage product suitability assessment principles.

In addition, FSRA will be issuing interpretation guidance outlining the expected approach to ensure suitability of a mortgage recommendation. Draft guidance will be issued for consultation in the fall of 2023.

Apart from strengthening industry standards, FSRA has introduced consumer education about private mortgages. The objective is educating consumers on the differences between a private mortgage and a traditional mortgage from a financial institution, what they should do if they are recommended a private mortgage, and what happens if they stay in a private mortgage for a long time.

FSRA expects to continue updating the consumer education content to keep it relevant for consumers as economic conditions change.

At the end of fiscal 2022-2023, FSRA started reviewing the conduct culture and compliance structure at large mortgage brokerages. As noted above, this focus was partly attributed to the increase in the number of licensed individuals with no corresponding increase in licensed firms.

As of March 31, 2023, FSRA licensed 2,881 mortgage brokers and 14,005 mortgage agents, compared to 2,833 brokers and 12,277 agents on June 30, 2019, representing close to 12 percent growth from 2019. This focus will continue into fiscal 2023-2024 (see section below). FSRA will report our findings in due course.

Other findings specific to our review of reverse mortgage and NQSMI brokering practices can be found in other FSRA materials. With the aging population and the rise in the number of reverse mortgages over the last few years,[6] FSRA expects to continue monitoring developments in this area.

Current market environment and trends

Mortgage affordability continues to decline with rising interest rates, inflation and home price correction

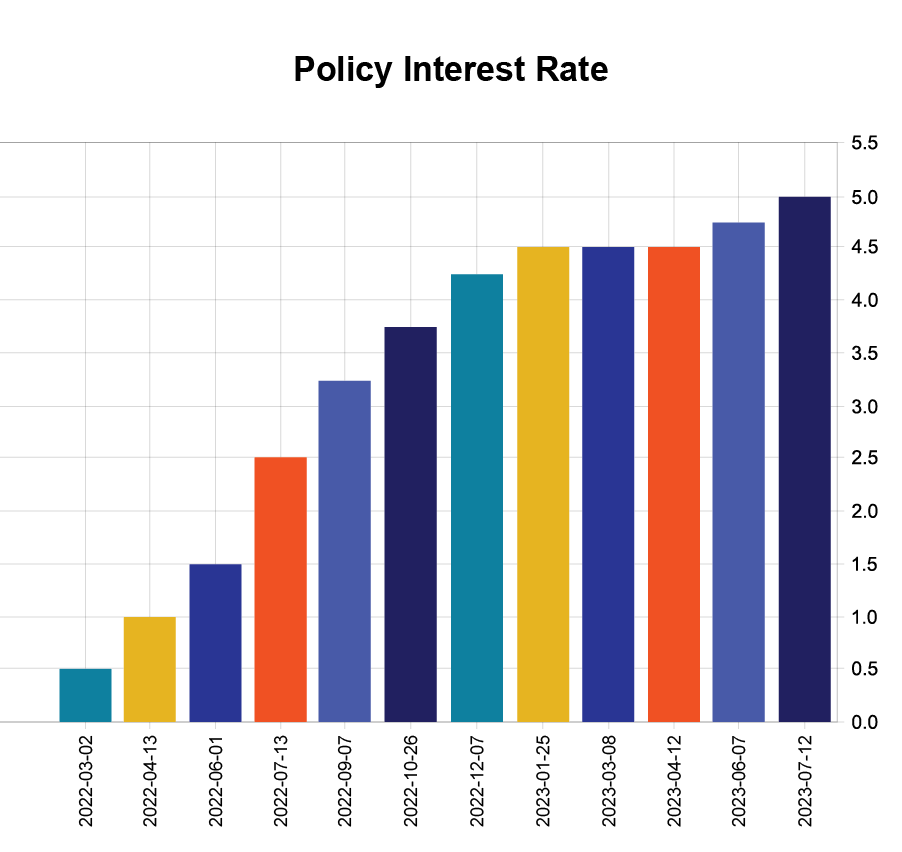

FSRA continues to observe declining mortgage affordability because of steep interest rate hikes. Since March 2022, the BOC has raised its policy interest rate ten times.[7] As of July 2023, the BOC’s policy interest rate sat at 5%. The BOC decided to increase the policy interest rate as persistent excess demand and elevated core inflation have made returning inflation to the 2% target slower than forecasted.[8]

Image

Source: Bank of Canada, Key Policy Interest Rate

The consumer price index (CPI), which is a measure of inflation rose 2.8% year-over-year in June. Mortgage interest cost remained the largest contributor to the increase.[9] With rising mortgage costs and housing price corrections,[10] consumers are taking longer to build equity in their homes. This reduces options on mortgage renewal and constrains the ability to refinance for more consumers.[11]

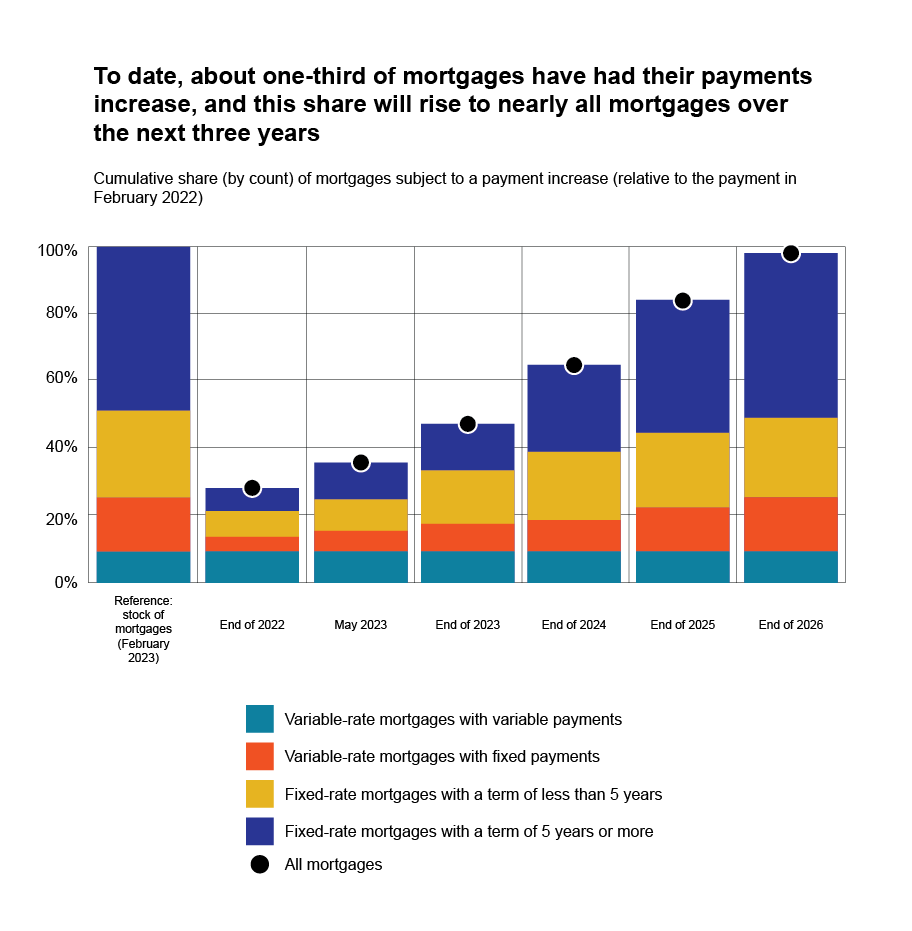

Based on the BOC’s analysis, by the end of 2026, nearly all mortgage holders will have seen their payments increase, and the median payment increase over the 2023–26 period will be about 20%.[12]

Image

Source: Bank of Canada, Financial System Review – 2023.

The BOC noted that indicators of financial stress remain low among households but are rising. As such, the BOC is concerned that reduced financial flexibility will make it increasingly difficult for consumers to service their debts.[13] At the same time, the Office of the Superintendent of Financial Institutions (OSFI) has raised concerns about mortgage lending risks and debt serviceability. OSFI has consulted on amendments to its Guideline B-20 on Residential Mortgage Underwriting.

Continued reliance on private mortgages by consumers

Given reduced mortgage affordability, we expect consumers will continue to rely on private mortgages.

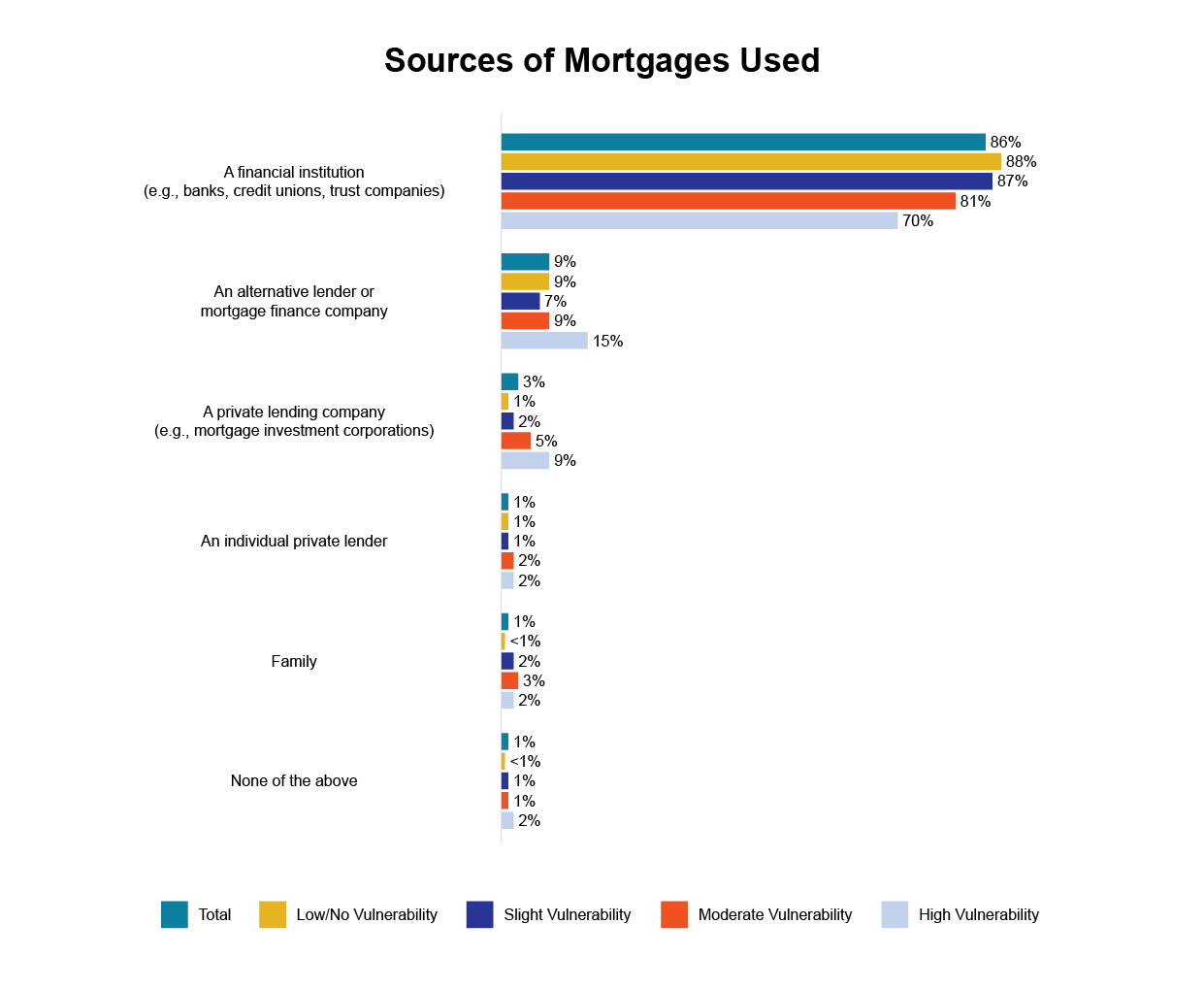

FSRA conducted a consumer survey in January 2023 of about 1,000 Ontario adults who have a mortgage. The survey results showed 13% of respondents have an alternative or private mortgage, one third of private/alternative mortgages are from mortgage investment entities and individual private lenders (see following chart).

Image

Source: FSRA 2023 Consumer Research Report.

Based on a preliminary review of data from the 2022 Annual Information Return (AIR), the value and number of total mortgages, and alternative and private mortgages brokered by licensed brokerages, stayed relatively steady between 2021 and 2022. However, there is an increase in higher ratio mortgages and lower ranking mortgages.

| AIR Data | 2022 | 2021 | % change |

|---|---|---|---|

| $ value of mortgages brokered and closed | |||

| Total | $193.1B (100%) | $193.0B (100%) | +0.1% |

| Mortgages from MICs, other MIEs and private lenders ($ and % of total) | $25.9B (13.4%) | $22.4B (11.6%) | +15.9% |

| High-ratio mortgages – all ($ and % of total) | $40.2B (20.8%) | $32.5B (16.8%) | +23.7% |

| High-ratio mortgages – insured ($ and % of total) | $36.3B (18.8%) | $29.4B (15.2%) | +24.4% |

| High-ratio mortgages – uninsured ($ and % of total) | $3.6B (1.9%) | $3.1B (1.6%) | +16.8% |

| Second or subsequent ranking mortgages ($ and % of total) | $8.4B (4.4%) | $7.0B (3.6%) | +19.7% |

| # of mortgages brokered and closed | |||

| Total | 341,291 (100%) | 346,165 (100%) | -1.4% |

| Mortgages from MICs, other MIEs and private lenders (# and % of total) | 39,565 (11.6%) | 36,568 (10.6%) | +8.2% |

| High-ratio mortgages – all (# and % of total) | 71,887 (21.1%) | 60,631 (17.5%) | +15.6% |

| High-ratio mortgages – insured (# and % of total) | 64,645 (18.9%) | 52,980 (15.3%) | +22.0% |

| High-ratio mortgages – uninsured (# and % of total) | 7,242 (2.1%) | 7,651 (2.2%) | -5.4% |

| Second or subsequent ranking mortgages (# and % of total) | 34,041 (10.0%) | 24,694 (7.1%) | +37.9 |

The rise in generally more costly and less standardized mortgages (i.e., private, high-ratio and low-ranking mortgages) continues to raise consumer protection concerns. FSRA is particularly interested in whether these mortgages are suitable for borrowers based on their unique needs and circumstances, and whether borrowers understand the features and implications of holding these mortgages. Knowing the true cost of borrowing, represented by the APR, will also be important for these borrowers.

A more challenging economic environment and more complex mortgages mean that licensed brokers and agents need to be more diligent to ensure consumer interests are top of mind. We also expect brokerages and their principal brokers to provide adequate oversight and training for their licensed individuals to ensure good outcomes for consumers.

Investor protection risks observed in mortgage investments

As the interest rate increases, mortgage investments may become less attractive. Housing market corrections, supply chain shortages, and increases in labour and material costs[14] mean performance of these investments, especially construction mortgages, are less certain.

In addition, according to a 2023 study by PricewaterhouseCoopers, lenders are tightening borrowing requirements with higher financing costs, making it harder for developers to raise capital and move projects forward.[15] When investors rely on administrators to manage investments in such conditions, we are concerned administrators are not being diligent enough. Potential issues include failure by administrators to monitor mortgage investments, especially in circumstances where there may be cost overruns for development projects, construction delays, and/or loan delinquencies. New disclosures should be issued by Administrators to provide timely updates to investors about the investments’ performance. These issues are especially concerning for less sophisticated investors.

Recent cases involving mortgage investments such as First Swiss Mortgage Corp and My Mortgage Auction Corp., highlighted other consumer protection risks, namely mishandling of investments or related funds for investors.

Areas of supervision focus 2023-2024

Reduced mortgage suitability and reliance on more costly and less standardized mortgages continue to raise risks that borrowers do not receive suitable mortgage recommendations for their needs and circumstances, or do not understand the features, costs or implications of holdng the recommended mortgage. Consumers might expect interest rates to decrease in the near term while industry experts generally feel that rates will stay high; therefore, brokers and agents play an important role in providing sound and objective mortgage advice to their clients.

For mortgage investors, the current higher interest rate environment introduces more uncertainty in the investment performance. For construction financing, there is the added risk that the underlying project does not progress as planned, negatively impacting the borrower/developer’s ability to make mortgage payments. When sophisticated and experienced lenders are being more cautious, intermediaries (like our licensed brokerages) may be tempted to solicit funding from retail investors. Mortgage administrators, especially if they are related to the developer or the intermediaries that arrange the mortgage, may not objectively inform investors of declining investment performance, and in the worst case mishandle the investments or funds for investors.

Protecting consumer-borrowers

FSRA will continue to focus its supervision in 2023-2024 on ensuring borrowers are protected in brokered private mortgages by assessing whether:

- Brokerages have adequate know-your-client processes

- Brokers and agents make suitable product recommendations

- Brokers and agents provide sufficient disclosure about mortgage features and implications

- There is adequate consideration of an exit strategy to ensure clients can transition back to more traditional financing

- There is adequate disclosure and management of conflicts of interest.

As noted earlier, in addition to supervision, FSRA will issue guidance on mortgage suitability to further clarify our expectations on how the sector can demonstrate that the mortgage recommendations they present to clients are suitable based on the client’s needs and circumstances. FSRA will also continue to build out our education content on private mortgages to support consumers who need to turn to private mortgages to finance their homes.

Since private mortgages are often more costly, with higher interest rate and additional fees (lender, late payment, renewal, foreclosure fees), FSRA will also assess whether all fees are being disclosed fully and clearly.

Moreover, having frequently seen understated APRs of borrowing[16] in previous examinations, FSRA will conduct a compliance blitz in fiscal 2024-2025. The blitz will concern APR disclosure made to consumers, with a focus on mortgage transactions completed in the 12 months before the blitz.

In the interim, brokerages and principal brokers should review internal practices and provide training when necessary. We expect to take action against any brokerages which exhibit systemic, or material deficiencies based on findings during the compliance blitz.[17]

FSRA started reviewing the conduct culture, compliance structure and principal broker’s supervision in large brokerages at the end of fiscal year 2022-2023. This program will continue. The objectives are to ensure all brokers and agents are conducting their activities with integrity and competence while keeping client’s interest in mind, supported by a strong conduct culture within the brokerage, and new agents are appropriately hired, trained and overseen.

A firm’s culture drives the norms, attitudes and behaviours of its management and staff. Conduct culture refers to a firm’s norms, attitudes and behaviours with respect to treatment of and outcomes for their customers. FSRA considers a firm with a strong conduct culture be one which takes actions and makes decisions that will not deliver poor or unfair outcomes for its customers harming their interests. A firm’s conduct culture impacts the risk of misconduct that can lead to poor or unfair outcomes for customers.

As part of a risk-based assessment of the effectiveness of a licensed brokerage’s compliance structure and its principal broker’s role, FSRA will obtain an understanding of the brokerage’s conduct culture. To do so, we will seek to understand what drives the behavior of the business and its people, specifically the following:

- The brokerage’s business strategy, specifically its business objectives, its “value proposition” or “competitive advantage” and target market

- The environment under which it operates (e.g., whether it is a competitive market)

- The compensation and performance expectations of the executives, its principal broker and other licensed individuals

- The philosophy and approach in hiring, attracting and terminating brokers and agents.

Protecting consumer-investors

Given the increased risk and uncertainty of certain mortgage investments and investor protection risks noted in recent cases, FSRA will examine the distribution and maintenance of mortgage investments by our licensed firms. FSRA will take an end-to-end approach to review practices from the point of sale to subsequent maintenance of mortgage investments, including practices of licensed or unlicensed firms related to a licensed brokerage or a licensed administrator that provide services to clients during the life cycle of the investments.

Our examinations will assess the following investor protection risks:

- Mishandling or loss of funds from mortgage payments

- Mishandling or loss of mortgage investments, when a mortgage is registered in a name in trust for the investor(s) or when an administrator has discretion over a mortgage

- Inadequate monitoring of mortgage performance and reporting to investors

- Failure to act in accordance with the mortgage administration agreement

- Failure to disclose and manage conflicts of interest when the administrator is related to the borrower of the mortgage they administer or to the brokerage that arrange the mortgage investment.

In addition, FSRA will finalize its proposed Guidance on Mortgage Administrator’s Financial Filing Requirements. The proposed Guidance will clarify existing reporting requirements and expand the scope of the required audit on compliance with specific MBLAA requirements. The objective is to protect funds and investments mortgage administrators handle for investors.

|

|

Key Risks |

Supervision Focus |

|---|---|---|

|

Unsuitable mortgage recommendations; consumers not understanding the features and true cost of borrowing |

Continue to examine private mortgage brokering to ensure:

Start planning for compliance blitz of calculation and disclosure of APR |

|

|

Ineffective compliance structure and principal brokers’ supervision at large brokerages |

Continue to examine conduct culture, compliance structure and principal brokers’ supervision in large brokerages to ensure that:

|

|

|

Mishandling of mortgage investments and related funds for consumer-investors |

Examine the practices of licensed firms and/or their related parties which provide services to investors during the life cycle of a mortgage investment |

[1] FSRA Consumer Survey Report.

[2] Data from 2022 annual information returns collected from licensed brokerages.

[3] July 12, 2023, Bank of Canada, Interest Rate Announcement.

[4] FSRA’s 2022 Consumer Research Study Executive Summary.

[5] 81% of mortgage transactions reviewed (56 of 69) in the MIC exams had no documentary evidence that a borrower suitability assessment had been performed (see MIC article in September 2023 newsletter); 56% (22 of 39) of private mortgage transactions reviewed in the first round of private mortgage brokering exams; and 65% (65 of 101) private mortgage transactions reviewed in the latest round of private mortgage brokering exams (see private mortgage article in September 2023 newsletter).

[6] Based on 2023 AIR data, the value of reverse mortgages brokered by mortgage brokerages has increased exponentially to $700M in 2023 from $268M in 2022 and $158M 2021, although still a small percentage of total mortgages brokered.

[7] July 12, 2023, CBC, Bank of Canada raises its key interest rate to 5%.

[8] July 12, 2023, Bank of Canada’s interest rate announcement.

[9] July 18, 2023, Statistics Canada, Consumers Price Index, June 2023.

[10] Based on Canada Real Estate Association, the average home price in Ontario declined by 1.1% in May 2023 from one year ago, and average home price in the Greater Toronto Area declined by 6.8% year over year in May 2023.

[11] Bank of Canada, Financial System Review – 2023.

[12] Bank of Canada, Financial System Review – 2023, Chart 12 and Chart 1-A.

[13] Bank of Canada, Financial System Review – 2023.

[14] PricewaterhouseCoopers, Emerging Trends in Real Estate 2023.

[15] Ibid.

[16] O. Reg. 191/08 prescribes how APR should be calculated and imposes certain disclosure requirements.

[17] See Mortgage Brokering Sector Newsletter issue 5.